No judgment. If you don’t automate your investments, that’s fine — but I want you to consider this:

What are your beliefs costing you?

For example, the people who don’t automatically invest often believe they have very good reasons:

“I like to have control”

“I don’t have a lot of money right now”

“I like to invest when the market is down”

Unfortunately, their beliefs will probably cost them hundreds of thousands of dollars over their lifetime. They think they’re doing the right thing, but they don’t know that if you miss the best 5 days of investing (over a 20-year period), your return would shrink from ~7% to ~5%.

That’s probably one of the costliest decisions they’ll ever make.

So, what are your beliefs costing you?

When I used to think I was just a “skinny Indian guy,” I believed that gym bros were dumb jocks who guzzled protein.

That single belief cost me years of looking better, learning the technicalities of fitness & nutrition, and cost me in personal relationships, too.

Think about these common beliefs. What are the costs of believing these things?

“College is a waste of money”

“I’m an introvert so I can’t do that”

“I have a slow metabolism so I can’t get abs”

I’m curious to hear from you.

I want to hear about a belief you had — and what it cost you. Share your belief in the comments section below.

But there’s a difference between manageable debt and unmanageable debt.

And you’ll know if you have unmanageable debt if:

You don’t know how much you owe.

You’re not paying off your statements in full each month.

You’re suffering psychologically from it (e.g., losing sleep, avoiding emails/phone calls from bank).

And unfortunately, there are a lot of people out there who want to take advantage of this. These are organizations that prey on people in debt in order to get money out of them — keeping them in debt longer.

Fortunately, there IS hope. Below I’ve outlined a system to help you reduce debt quickly and also give you a look into debt reduction companies so you can make the best choices for you.

What is debt reduction?

Debt reduction is taking proactive measures to cut down the money you owe to creditors. This includes things like:

Credit cards

Student loans

Car loans

Mortgages

Utility bills

Rent

And there are actually debt reduction services out there that’ll help you with this. They’ll work with your creditors to either A) consolidate your debt, B) negotiate with your creditors to lower your payments, or C) a combination of both.

Note: Debt consolidation is the process of using one loan in order to pay off all of your debt. That loan has a lower interest rate than your debt. So in theory you’ll end up paying less because you’re not paying as much in interest.

On the surface, they can seem like a gift from heaven. Angels sent by God to help lift you out of debt forever. What could be better?

Well, there are a LOT of pitfalls that can come with them.

I’ve talked about this before in my article about debt consolidation — but the short of it is this: Many of these companies prey on people in debt in order to get money out of them for as long as they can.

There are a lot of issues with this, but the three biggest ones are:

You’ll be in debt longer. Even the scammiest consolidation services will be able to give you a lower interest rate on your loan. However, they often protract your loan term (the length of your loan), meaning you’ll be in debt longer and end up paying more even with lower interest rates.

You might lose a BIG asset. If you put your car or home down as collateral and fail to make payments, your debtors are within their rights to repossess those assets. Losing a car could mean your livelihood is at stake if you commute to work. And having a house taken away from you could mean homelessness.

Your credit score will drop. 15% of your credit score is how long you’ve held onto a line of credit for. That means if you pay off a bunch of credit and take on a single big loan, you’re going to see a drop in your score. That drop only gets bigger with the more lines of credit you close.

That said, there ARE good debt reduction services out there. The trick is to find a good one that’ll fight for you — instead of squeeze you for all the money you have.

How to find a good debt reduction service

If you want to find a good debt reduction service, look for a non-profit.

These are 501(c)(3) organizations that help provide debt relief through things like:

Consolidation

Credit/debt counseling

Negotiating lower interest rates or total payment with your creditors

Since they are non-profit organizations, these debt reduction services are funded through grants and donations — meaning they’ll cost you little to nothing to use their services.

There are still scammers to be wary of (even in the non-profit world). So to make sure you find a reliable debt reduction service, you’ll need to look out for a few things:

Fees. Yes, you read that right. Reputable non-profit debt reduction services will charge you a fee. These are typically monthly maintenance fees that are relatively low cost. Note: A good non-profit will work with you if you cannot afford it. Some will even waive the fees entirely for you.

Non-profit status. “Well, no duh,” you’re probably saying. But the reality is a lot of scammers pretend they’re non-profit in order to take advantage of people’s goodwill.

Spend the next week calling them and asking them about their fees, proof of their non-profit status, and what they can do for you.

A good non-profit will spend about an hour on your consultation. Beware of any organization that wants to take your money and put you into a plan right away. They are NOT looking out for your best interests.

Below is our process to help you eliminate debt for good. We go more into this system in our article on how to get out of debt fast — but I’ll give you a solid rundown of it below so you can get started as soon as possible.

Because if there’s one important thing when it comes to getting out of debt/investing/saving/earning/anything finance related, it’s this: It’s best if you do it early, often, and consistently.

It all boils down to human nature. Debt is a bad thing. Society looks down on people who owe exorbitant amounts of money. So people end up feeling guilty about their debt.

So what do we do? One of two things:

Blindly pay the minimum amount toward bills with no strategy.

Not pay at all because we’re paralyzed by our debt.

You play right into the creditor’s hands when you do this. They’ve designed the system so it’s easier for you to just send in the minimum payment or avoid paying entirely. When you do this, they end up getting MORE money.

You need to fight against this BS. And the first step in doing that is finding out exactly how much you owe. In the end, you’ll probably find that it’s not as bad as you anticipated.

ACTION STEP: Find out how much you owe across all of your debt.

Spend the next hour finding out how much debt you owe. This means calling up your credit card companies or digging up a recent statement. Logging onto your student loan portal to see how much you owe. Or emailing your mortgage lender. Whatever it takes to find out how much you owe.

Add up all of the numbers on a spreadsheet and you’ll have a solid idea of how much you owe.

Once you do that, congrats! You’ve taken the hardest and first step in getting out of debt.

Here’s a handy spreadsheet template you can use to calculate your debt.

DEBT

TOTAL OWED

APR

MONTHLY MINIMUM PAYMENT

Credit card A

$X

X%

$X

Credit card B

$X

X%

$X

Student loan

$X

X%

$X

By finding out exactly how much you owe, you can start to strategically approach taking down your debt.

Step 2: Decide what to pay first

Now you need to ask yourself: Which debt should I pay off first?

And there are a lot of different ideas on how this should be approached.

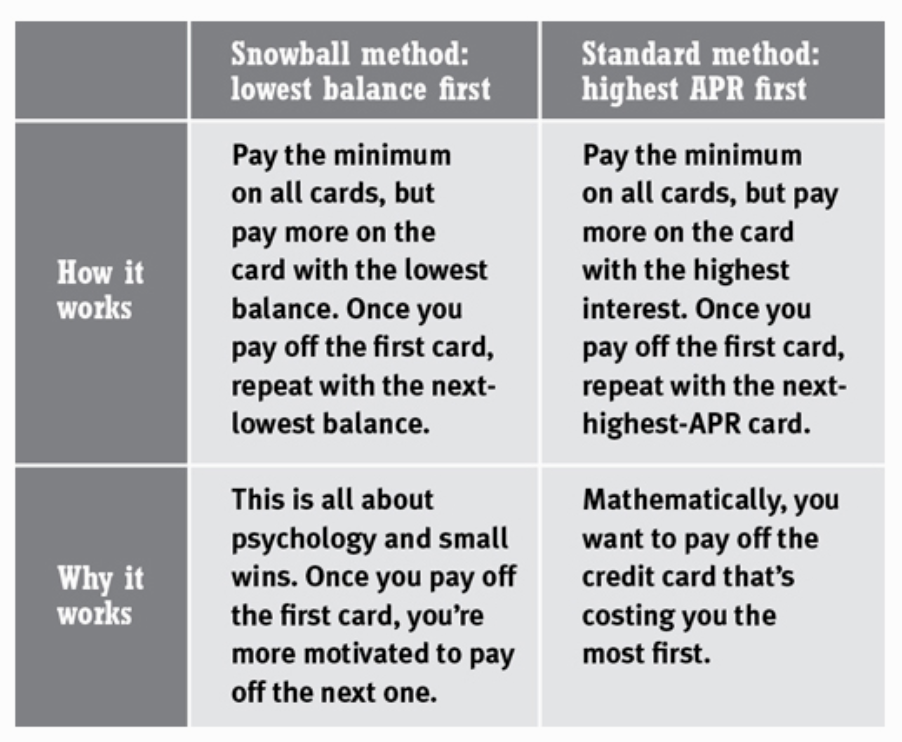

The standard method involves paying the minimum on all debt, but pay more money to the loan with the highest APR because it’s costing you the most.

Dave Ramsey famously touts his Snowball Method of getting out of debt. This involves paying the minimums on all of your debt, but paying more money to the card with the lowest balance first (i.e., the one that will allow you to pay it off the quickest).

This is a source of fierce debate in debt reduction circles. Technically, this method isn’t the most efficient way to approach your debt since the debt with the lowest balance doesn’t necessarily have the highest APR. Psychologically, it’s very rewarding to see one debt paid off. That’s why it’s the one I suggest.

For more on this, check out my video below.

ACTION STEP: Choose a debt reduction strategy.

It doesn’t actually matter too much which method you choose. The important thing is for you to choose one.

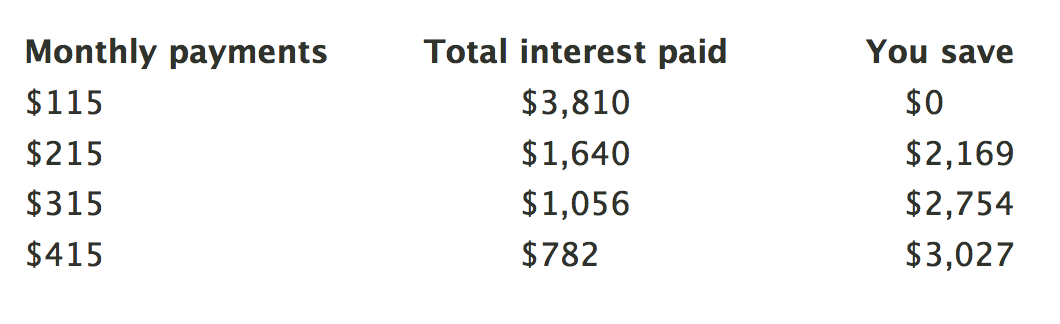

Pro tip: When it comes to your student loans, you can actually save thousands of dollars each year — by paying down your debt more each month.

Let’s say you have a $10,000 student loan, at a 6.8% interest rate, and a 10-year repayment period.

If you go with the standard monthly payment, you’ll pay around $115/month.

But check out how much you can save per year if you paid just $100 more each month:

Even $20 more per month can save you huge amounts of money.

I’m a huge fan of taking 50/50 odds if the upside is big and it only takes five minutes of my time.

That’s why I love negotiating my interest rates. The best part is it works surprisingly often — and if it doesn’t, so what? Especially considering you can save more than $1,000 with a single phone call.

Remember: Negotiations are all about being polite yet firm. Remind them that you’re a loyal customer and appreciate their service — but you’d really like to have your interest rates lowered to help you pay off debt.

ACTION STEP: Use this script to lower your APR.

Here’s a word-for-word script that many of my readers have used already to lower their interest rates:

YOU: “Hi, I’m going to be paying off my credit card debt more aggressively beginning next week, and I’d like to lower my credit card’s interest rate.”

CC REP: “Uh, why?”

YOU: “I’ve decided to be more aggressive about paying off my debt, and that’s why I’d like to lower the interest rate I’m paying. Other cards are offering me rates at half what you’re offering. Can you lower my rate by 50% or only 40%?”

CC REP: “Hmmm … after reviewing your account, I’m afraid we can’t offer you a lower interest rate.”

YOU: “As I mentioned before, other credit cards are offering me zero percent introductory rates for 12 months, as well as APRs that are half what you’re offering. I’ve been a customer for XX years and I’d prefer not to switch my balance over to a lower-interest card. Can you match the other credit card rates, or can you at least go any lower?”

CC REP: “I see … hmm, let me pull something up here. Fortunately, the system is suddenly letting me offer you a reduced APR. That is effective immediately.”

Repeat this process for any other cards you can, and then move on to my favorite step.

Step 4: Find the money to pay off your debt

One common barrier to paying off debt is wondering where the money should come from. Balance transfers? Using money from your 401k or savings?

These questions are daunting — which is why I want to address two bad options now and give you some good ones:

Balance transfer. Many people begin by considering a balance transfer to a card wit a lower APR. I’m not a fan of this. Why? Simple: It’s a Band-Aid for a larger problem (typically your spending behavior). Plus the process is very confusing, rife with tricks pulled by credit card companies to trap you into paying more. A better option would just be to negotiate down your APR.

Using money from your 401k. This is also not a viable solution. Not only do you put your financial future in serious jeopardy by borrowing against your 401k, you’re setting yourself for a bad habit of dipping into these accounts whenever you fall into debt. Plus you’ll be heavily penalized if you withdraw from your 401k before retirement age — losing even MORE money. I repeat, do not use money from your 401k.

Instead, I recommend you try four things:

Use the cash you’ve freed up from Step 3. You’re paying less in interest now and should use that money towards taking down your debt.

Set up a Conscious Spending Plan. This is an automated system that lets you know exactly how much you have to spend each month — while also paying off your debt automatically.More on that here.

Tap into Hidden Income. Through more negotiations, you’ll be able to save hundreds per year on things like cable, cell phone, utilities, car insurance, and even rent. More on that here.

Earn more money. This is my favorite way of getting out of debt. You can only save so much money — but there’s no limit to how much you can earn. More on that here.

Beating debt isn’t easy — but through a few straightforward systems, you’ll be able to take control of your debt for good and build habits that’ll lead to financial success.

Do me a favor: Write in the comments below one thing you’re going to do TODAY to help get you out of debt. I’d love to hear from you.

There’s no secret to buying a house — but it does involve thinking differently than most people.

I’m talking about the people who make the biggest purchases of their lives without fully understanding the true costs. If you do so, you’ll undo years of hard work in other areas of your financial life.

Luckily, there’s a good rule of thumb to help you find out exactly how much you can afford: The 28/36 rule.

Find how much house you can afford with the 28/36 rule

The 28/36 rule is used by lenders to determine how much house you can afford — and it’s pretty straightforward:

Maximum household expenses shouldn’t exceed 28% of your gross monthly income. This includes everything within your home mortgage.

Total household debt shouldn’t exceed more than 36% of your gross monthly income. This is also known as your debt-to-income ratio.

Let’s break down each of those areas now a little bit more. That way, you’ll have a better idea of what lenders are looking for.

Maximum household expenses

All of the expenses that make up your monthly mortgage payment are also known as the PITI:

Principal. This is the part of the payment that goes towards paying down the amount you borrowed to purchase the house.

Interest. This is the rate creditors charge for lending you the principal.

Taxes. This is your property tax.

Insurance. This is your homeowner’s insurance.

When you take the amount you owe towards your PITI and compare it to your income, you have your “front-end ratio.” This number is what most lenders look at when determining how much they’ll lend to you.

Dollar amount of your PITI÷ Dollar amount of your gross monthly income = Front-end ratio

And then:

Front-end ratio x 100 = Front-end ratio percentage

With the 28/36 rule, you’ll want your PITI number to be less than 28% of your gross monthly income. Use this formula to find out exactly how much house you can afford.

For example, if your gross monthly income amounts to $4,000 / month, the best mortgage you’re likely to attain would amount to no more than $1,120 / month since that’s 28% of your income.

Total debt

Like your front-end ratio, your debt-to-income ratio is also worth calculating if you plan on getting a home mortgage.

Unlike your front-end ratio (which compares the amount you owe on your house to your income), this number compares your income to your debt. Creditors look at this number to determine how risky it is to lend to you.

The riskier it is to lend to you, the smaller chance you have of attaining a home loan — or at least a home loan with a good interest rate.

Much like your debt-to-asset ratio, calculating it is simple:

Dollar amount of monthly debt you owe÷ Dollar amount of your gross monthly income = Debt-to-income ratio

And then:

Debt-to-income ratio x 100 = Debt-to-income ratio percentage

Say you owe about $1,000 in debt month-to-month and make $75,000 a year ($6,250/month). We’d then take 1,000 divided by 6,250 in order to get our debt-to-income ratio, like so:

1,000÷ 6,250 = .16

Multiply .16 by 100 and you have 16% for your debt to income ratio … but what does that number mean?

The lower the number is, the better. While the 28/36 rule-of-thumb says that you should ideally have no more than 36% for your debt-to-income ratio, most lenders will provide you a mortgage up to 49%.

So if your debt-to-income ratio amounted to 16% like in the example above, you’d be in good shape for a loan.

IWT’s suggestion: Be as conservative as possible

When it comes to personal finance, I like to be aggressive in certain areas, like investing.

However, when it comes to real estate, I’m typically as conservative as possible. That’s why I urge you to stick to tried-and-true rules like 20% down, a 30-year fixed-rate mortgage, and a total monthly payment that represents no more than 30% of your gross pay.

If you can’t do that, wait until you’ve saved more.

It’s okay to stretch a little, but don’t stretch beyond what you can actually pay. If you make a poor financial decision upfront, you’ll end up struggling — and it can compound and become a bigger problem through the life of your loan.

Don’t let this happen, because it will undo all the hard work you put into the other areas of your financial life.

If you make a good financial decision when buying a house, you’ll be in an excellent position.

How to save thousands towards a house

Have you ever gone to buy a car or cell phone, only to learn that it’s way more expensive than advertised? I know I have, and most of the time I just bought it anyway because I was already psychologically set on it.

But because the numbers are so big when purchasing a house, even small surprises will end up costing you a ton of money.

For example, if you stumble across an unexpected cost of $100 per month, would you really cancel the paperwork for a new home? Of course not. But that minor charge would add up to $36,000 over the lifetime of a 30-year loan — plus the opportunity cost of investing it.

Remember that the closing costs — including all administrative fees and expenses — are usually between 2% and 5% of the house price. So on a $200,000 house, that can be $10,000.

Keep in mind that ideally the total price shouldn’t be much more than three times your gross annual income. (It’s okay to stretch here a little if you don’t have any debt.) And don’t forget to factor in insurance, taxes, maintenance, and renovations.

If all this sounds a little overwhelming, then good. It should be. This is likely the biggest purchasing decision of your life. That’s why you need to research as much as you can before you dive in.

To help you with that, be sure to check out my very best resources below on the topic:

How to buy a house. We break down the five exact steps you should take in order to buy a house.

Intro to real estate investing. I give you the myths surrounding real estate and also the systems to get started with investing.

7-part real estate primer. My friend Owen Johnson breaks down the intricacies of real estate in seven awesome articles.

For now, though, I want to show you a system to help you save money painlessly for a house.

How to save for a down payment

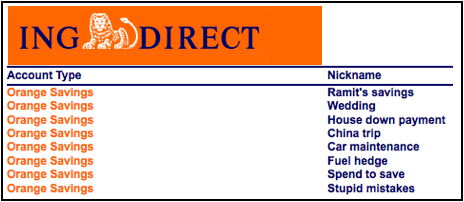

Instead of skipping lunches, cutting out lattes, or canceling your Netflix membership, I suggest you leverage the power of a sub-savings account.

These are accounts that you can create within your normal savings account for specific purchases.

This is how you can accomplish savings goals passively because you don’t see the money when it transfers. It’s automatically withdrawn from your checking account and put towards your specific savings goals. You’ll never miss it!

To set one up, you need to have a savings account that lets you set up sub-savings accounts with it.

I use Capital One 360 (formerly ING Direct). I talked about this bank account in my New York Times best-selling book I Will Teach You To Be Rich over 10 years ago, and I STILL use the same account now.

But it doesn’t really matter which savings account you choose as much as just getting started. So don’t spend too much time deciding which one to go with.

Once you set one up, you can even name these accounts to reflect your goals.

When I first discovered sub-savings accounts, I created one and named it “Down Payment” for a down payment on a house. I was regularly transferring money into it based on my savings goals using my automated finances.

As the months passed, the amount in that account grew, and I felt really proud of my accomplishment.

During this time, one of my friends was just blindly putting away money in an account he had mentally earmarked for vague goals.

Though we might have had the same amount saved away, the difference between us psychologically was staggering. Where he felt despair about trying to save money, I was motivated.

For me, I wasn’t working towards $20,000 for a down payment. I was working on saving $333 a month over five years — a perfectly achievable goal, especially after I tracked my progress.

Eventually, my friend did open up his own sub-savings account. He told me that doing so changed his entire perspective on saving money for the better.

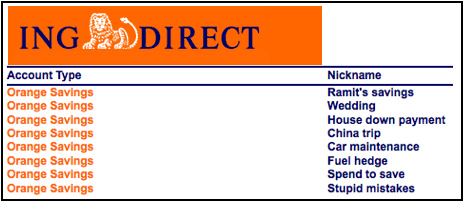

Check out all the different sub-savings accounts I had in my old savings account.

ING Direct is now Capital One 360. BTW that wedding one is going to be put to good use.

Here’s a look at a few sub-savings accounts I have now:

ING switched to Capital One 360, and I used the money I saved to buy an engagement ring.

Once you have your sub-savings accounts open, it’s time to automate the entire system.

Automated finances are the ultimate cure to never knowing how much you have in your checking account and how much you can spend.

When you receive your paycheck, your money is funneled to exactly where it needs to go — whether that be your utilities, rent, Roth IRA, 401k, or your savings account.

Check out my video below to learn exactly how to set it up today.

Earn money for your future home

I suggest putting around 5% of your income into your sub-savings account each month for your house. Though this amount seems small, you’re going to be surprised at how easily it will add up over time.

Luckily, you can make that 5% even bigger. How? Simple: Earning more money.

I’ve said it once and I’ll say it a thousand more times: There’s a limit to how much you can save but no limit to how much you can earn.

That’s why my team and I have worked hard to create a guide to help you earn more today:

The Ultimate Guide to Making Money

In it, I’ve included my best strategies to:

Create multiple income streams so you always have a consistent source of revenue.

Start your own business and escape the 9-to-5 for good.

Increase your income by thousands of dollars a year through side hustles like freelancing.

Download a FREE copy of the Ultimate Guide today by entering your name and email below — and start earning more towards your house today.

Here’s a free budgeting workbook to help you get your finances on track! Whether you’re starting from scratch or you’ve had a working budget for years, this simple 2-page workbook will help you categorize and visualize where your money is going. This will help you make better decisions with it! Why You Need a Budget [...]

Hi, I’m New York Times best-selling author Ramit Sethi, and I’m going to show you how to make more money fast, legitimately, and with immediate results.

This is easily one of my most popular articles. That’s why I’ve updated this article to include the very best tips on how to make money for 2018.

For the next six minutes, I’ll teach you how to earn more money after one conversation with your boss, how to lower every single one of your bills, and how to start making money with a side hustle THIS WEEK.

Then we’ll get into how to optimize your career and job – the easiest way to make the most money FOREVER.

Quiz: What is your earning potential? Choose the answer you agree with the most

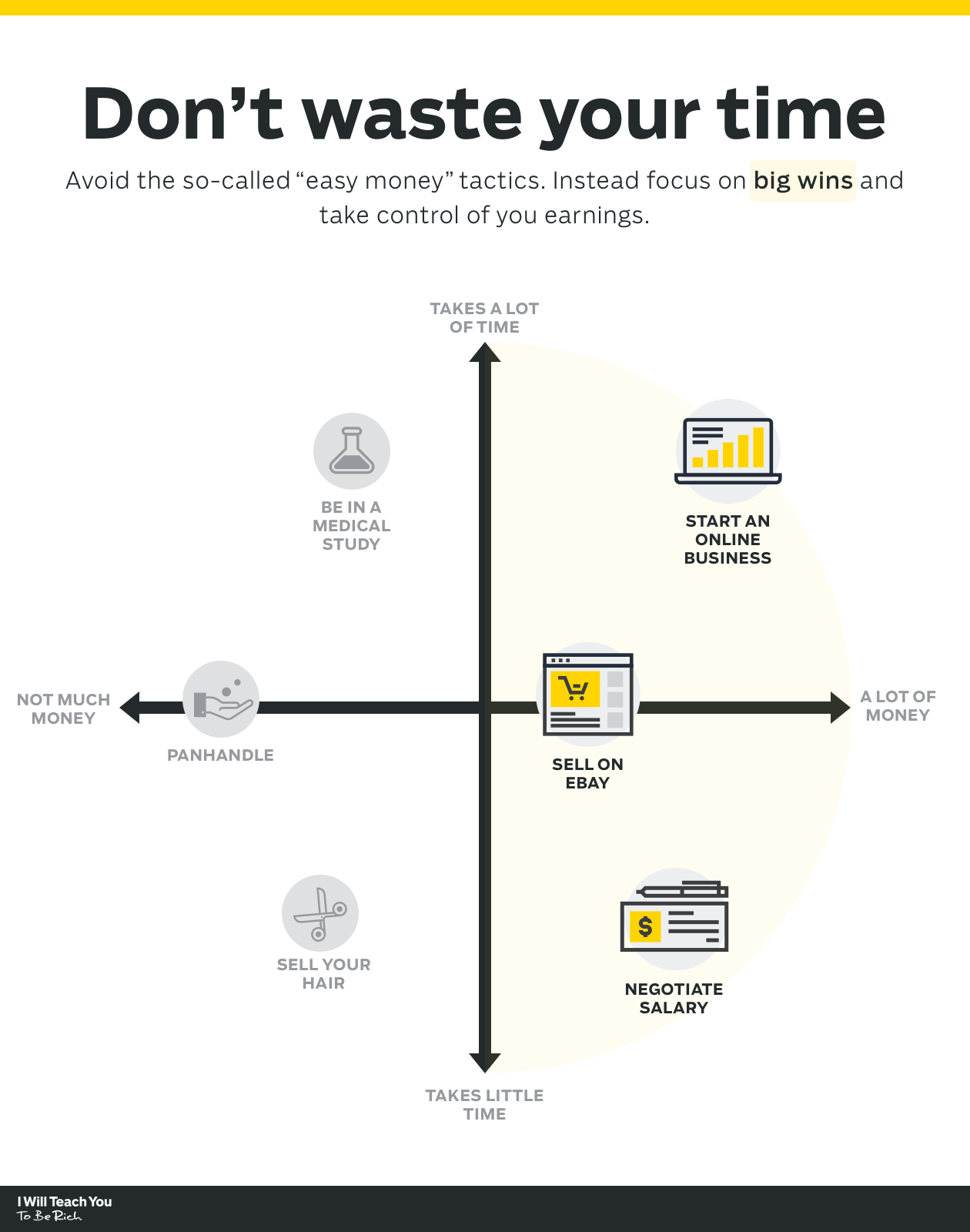

We’re going to focus on Big Wins. That means clear, actionable advice that you can start implementing today.

That means we’re not going to tell you to:

Take online surveys for literally tens of dollars

Sell your plasma/hair for quick cash

Cut out lattes or skip lunch to save money

These are what I call Big Wins — the types of strategies that will show you how to earn money while setting you up for long-term success. But long-term does not mean “delayed.” There are easy ways to make quick money. But you need to think big.

That’s why we’ll tackle this in two, equally important sections.

Section 1: How to make money THIS WEEK. Non-scammy ways you can make more money fast to get your head above water within seven days. Note: All of these have LONG-LASTING effects.

Section 2: How to make money FOR THE REST OF YOUR LIFE. Long-term systems to dramatically increase the money you make in your LIFETIME. My students have gone from starting freelance gigs on the side all the way to six-figure businesses. They’ve also tripled their salary in a matter of months.

This is a long post with a lot of information. Follow the instructions below and we’ll show you where you should focus your efforts:

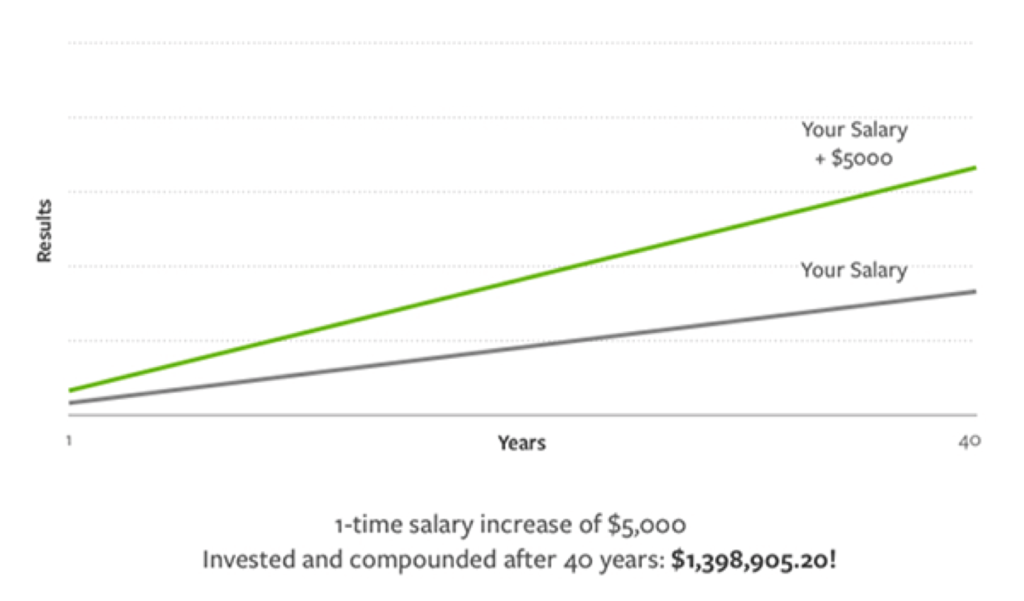

With just a five-minute conversation you can make thousands more and, what’s better, the gains add up year after year.

This is a proven way to earn more money through a single conversation. It’s essentially quick money that — unlike taking surveys or selling your body to medical studies — gives you a LOT of money over many years.

Check this chart demonstrating the effects of ONE $5,000 raise:

Learning how to make more money via salary negotiations is simple — though it’s going to take a little bit of work on your part:

Step one: Find out! Use sites like PayScale.com, Salary.com, or Glassdoor.com and get the salary range for your job and location.

Step two: Give the heads up. Let your boss know you’re preparing to discuss salary with him or her. I cover how to do that in the 14-minute video below.

How to negotiate your salary

Step three: Use the Briefcase Technique. Before even stepping foot into the room, use my tried and true Briefcase Technique. This is something my students have used THOUSANDS of times for IMMEDIATE gains in salary.

The Briefcase Technique

Now, two big roadblocks might arise.

First, if you’re not good at your job, there’s no amount of negotiating that will help.

That’s why I love salary negotiations. Not only is it a good incentive for you to work harder and become a Top Performer, but you also stand to gain a lot of money from the hard work.

FACT: Doing a good job at work 10x’s your chances of making more money.

But if you’re going through your job just HOPING you’re doing a good job, you’ll be forgotten when it comes times for raises — and you won’t earn more.

Just like great companies get inside the heads of their customers, Top Performers figure out EXACTLY what their bosses want and optimize their strengths accordingly.

Tie everything you do to whatever goal is important to your boss and remind them often. This is how people become indispensable.

See my interview with Michael Williams for more:

Second, your company might tell you that they simply don’t have enough money to give you a raise. Get around that stonewall using the systems I outline in the video below.

Ask Ramit: How can I negotiate salary when they tell me they can’t pay more?

Once you have all of your prep ready, you’re good to go. But if you’re a weirdo overachiever like me, you can also check out my complete guide with scripts, more videos, and common mistakes here.

Negotiating your salary takes a bit of upfront work, but just ONE conversation can be worth thousands. It’s one of the easiest ways to make money.

The best way to make money fast is not to reinvent the wheel and to leverage the sources of income you already have. So the next time someone tells you to get more money by cutting back on lattes or by picking up loose change, grab them by the shoulders, and shake them for me.

Be sure to remind them that you’d have to skip out on 1,370 lattes in order to save $5,000 (or they can just get a one-time raise).

The awesome thing about negotiations is you can do it with practically every service you pay for. That includes the fixed costs you pay each month.

Things like:

Credit card rates and fees

Gym fee

Cable fee

Cell phone fee

Car insurance

With a quick phone call you can get these costs lowered, putting more money directly in your pocket.

Because the dirty secret is that most of these companies rely on thousands of people to zombie walk through their payment process. That’s why your cable company seems to jack up rates every year. They know you’ll likely just shrug, throw it away, and carry on with your day.

NOT TODAY!

Save $1,000 with 5 phone calls

By calling these companies and asking one simple question, you open the door for more money in your pocket. Just remember two magic phrases:

“Times are tough.”

“Is there anything you can do for me?”

Example conversation:

You: Hi, I was looking at my plan and it’s getting pretty expensive. Could you tell me what other plans you have that would save me money?

Them: Blah blah same plans as on the website blah blah

You: What about any plans not listed on the website?

ThemNo, what we have is listed on the website. Plus, you’re on a contract and have an early cancellation fee of $XXX.

You: Well, I understand that, but I’d be saving $XXX even with that cancellation fee. Look, you know times are tough so I’m thinking of switching to [COMPETITOR COMPANY]. Unless there are any other plans you have…? No? Ok, can you switch me to your cancellation department, please?

The key is to be nice. Be cordial and ask them what better plans they have to offer you. Nothing’s going to get you shot down quicker than getting angry and screaming, “HOW DARE YOU SCREW ME OVER WITH THESE PRICES. I WON’T STAND FOR IT. GIVE ME LESS FEES … uh please?”

If you mess up or things don’t go as planned, don’t worry. Hang up and call back. You can always play around with a few phone calls and see what works best.

When you get to the customer-retention department, restart the sequence. This is when you pull out your competitive intel on the other services being offered.

If Verizon is offering something for $10 less, tell them that. That’s $120 savings / year right there. But you can do more.

You: Listen, you know times are tough and I need to get a better deal to stick with you guys. You know and I know that your customer acquisition cost is hundreds of dollars. It just makes sense to keep me as a customer, so what can you do to offer me this plan for less money?

Notice that you didn’t say, “Can you give me a cheaper plan?” because yes/no questions always get a “no” answer when speaking to wireless customer service reps (or anybody whose job it is to get you off the phone and out of their hair as soon as possible).

Instead, ask leading questions. You also invoked the customer-acquisition cost, which is meaningful to retention reps. Finally, it really helps if you’re a valued customer who’s stuck around for a long time and actually deserves to be treated well.

I’ve said it before and I’ll say it again: There is a limit to how much you can save, but there is no limit to how much you can earn.

Finding a new job or changing careers takes time (we’ll get to that). But in the next few days you can set up your first side hustle and make money fast.

The best part: Freelancing is a skill. That means you can get BETTER at it with time.

And once you get your first paying client, it’ll be easier to get more clients and make more money.

First thing: So many other websites will tell you to troll for freelance gigs on places like Elance or Mechanical Turk. These places work if you want to compete with people all over the world in a race to do the most work for less. No thanks.

Look at what you’ve already got. 95% of jobs can translate into some sort of side gig. Ask yourself:

What do I enjoy?

What do I do with my free time?

What do people ask me to do because I’m so good at it?

People are very bad at identifying their own skills. They’ll say things like, “I dunno … I guess I’m good at writing and communication, and, like, general organizational skills…” AMAZING!! HERE’S A $4,000/MONTH RETAINER!!! (Sorry, won’t happen.)

Repeat this over and over: People pay for solutions, not your skills.

For example, I was on a webcast where I was suggesting ways for people to earn money on the side, and I mentioned that I hate cooking, am not good at it, and would love it if someone cooked for me.

I got an email later that night from someone who said, “Ramit, I can help. I can teach you everything you need to know over one weekend, and you’ll know 3-5 great dishes to cook.” I appreciated the offer, but wrote back, “Thanks for the offer! But you don’t understand. I don’t want to learn — I want someone to do it for me.”

Again: People have problems. And they want solutions.

They don’t care what you’re “interested” in. Are they too busy to organize their closet? Do they need someone to help them redesign their website? Maybe they want someone to teach their kid how to play flute.

Start off by assessing the skills you use every day at home or at work.

Typically, you can break these down into two areas:

Skills. These are things you have expertise and knowledge in (e.g., languages, coding, copywriting).

Passions. These are things you love to do in your free time (e.g., playing musical instruments, volunteering to take care of animals, genealogy work).

Take some time right now to write down 10 – 20 ideas of different skills and talents you have.

After you’re done, let’s take a look at an example of this in action. Maybe your list looks like:

Do a little PHP coding

Organize systems

Automate complex processes

Project manage

Create technical documents that can be understood by lay audiences

Lead a team

Now ask yourself: Which of these skills can solve a specific problem? Brainstorm those out. Don’t censor yourself — put everything down.

I could do some PHP coding, but I’m not the best.

I could help businesses automate and streamline their income-generating processes. Vague, but okay.

I could manage projects and lead teams towards deadlines / organizing. This is super vague, any 22-year-old college grad would say he could do the same, and it doesn’t take advantage of my specific skills. Skip this.

I could be a technical writer and help companies demystify their technical-support documents. I could even rewrite the technical portions of their websites to make them more comprehensible to normal people, especially companies in the consumer energy field. Very promising, especially since I follow a few of these companies online.

Each of these individually is a potentially viable freelance trade – can you pick one and do it? The answer should be YES/NO to each. Put “YES” if even remotely feasible.

PHP coding: YES

Automate systems: NO (too vague for me to know where to start)

Project manage: NO (too vague)

Technical writer: YES

Excellent. Now you have a list of skills that might potentially be profitable.

Optional: Combine skills together to make a more compelling, more niche offer.

You can often charge more and help clients more by packaging offers. In this case, it’s not very relevant, since technical writing and PHP coding are pretty different. But one of the people who helps on IWT pitched me to do video editing + marketing. Perfect fit. I hired him.

Next step: How can you prove to people that you’re knowledgeable enough for them to pay you?

The first thing I do when evaluating someone is look at their portfolio and past clients. At least half of potential hires don’t have this section. Easy solution! I move on to someone who does.

For our systems engineer, can he point to a PHP project he did on the side?

What about a sample of technical writing where he turned something very complicated into something totally palatable?

Last step: Start finding clients. With your offering in place it’s time to find potential clients. Sure you could randomly print business cards or set up a blog. But before doing ANY of that you need to make sure you have something people want.

– Identify your clients. Who are they? What are their hopes and dreams? How old are they? What do they do? Are they married? How big is their company? (More on getting your first 3 clients here.)

– Reach out directly. Lots of people set up a Twitter account and wait for the world to come to them. DON’T DO THAT. Once you’ve identified your potential client, email them directly. Example email:

Hi Mike,

My name is Ramit Sethi and I’m a recent Stanford grad. I’ve been reading your blog for two years (I loved the post about using virtual assistants and got BOTH of my brothers to start using one), and it’s really helped me be more efficient with my work.

It occurred to me that you’re probably interested in growing your blog. I might be able to help. I’ve done video editing (https://ift.tt/2vXDo7q) and PowerPoint design (https://ift.tt/2wx6lKM). Imagine doing a great video on using virtual assistants, then distributing it through your newsletter. I could do one for you in about 2 days if you’re interested.

How about chatting later this week? My # is XXX-XXX-XXXX or I can give you a call at your convenience.

Thanks,

-Ramit

This email script has generated thousands of dollars for my students and can help you connect deeply with your potential clients and begin a relationship that can lead to your first paying client.

Want more? I have an entire course on how to earn your first $1,000 on the side.

Money tip #4: Negotiate your rent

I’d bet that rent is your biggest expense. Save $100 on your rent and that adds up to $1,200 a year with ONE conversation. Or you could collect 24,000 cans and recycle them. Your choice!

Of course, you can’t just say, “I want to take $200 per month off my rent!” You have to be ready to offer something in return.

What does your landlord really want? Money, of course. But dig deeper and you’ll find there’s a lot more you can offer. The goal is to give them something you don’t care about in exchange for something you do.

Here are a few things many landlords will happily lower rents for:

Prepay months in advance

Sign an extended lease

Offer to extend the termination notice from 30 days to 60 or 90 days

Offer to give up your parking space if you don’t have a car (the landlord could charge another tenant for an extra space)

Promise not to smoke in the apartment (this will save the landlord money when you move out)

Promise not to keep cats even if they’re allowed (another cleaning expense for the landlord)

Make a deal for referrals if they have low occupancy

If you know what you want and you know what they want, the chances of succeeding in your negotiation increase significantly.

Hi Jim,

I hope you’re enjoying the start of summer in the Bay. Since our 1 year lease is almost up, I’d like to chat about re-signing.

As you know, I love the apartment. I’ve gotten to know the neighbors and feel truly at home in the neighborhood. I hope to be able to stay here for a while yet.

I’ve been looking at rental prices around the area, and would like to talk with you about adjusting the rent to match what I’m seeing around town.

I’d also be more than happy to help out around the property — taking out the trash and recycling, clearing and cleaning the backyard, or any other duties that might need some attention. I love living here and hope that the relationship with you and the property is just beginning.

I can chat on the phone any time you’re free today or this weekend.

Talk to you soon,

Susan

Section 2: Make more money FOR THE REST OF YOUR LIFE

Negotiating your salary, bills, and picking up some side work are all quicker wins. But while your motivation is high, you can also begin some larger efforts with a few of my favorite systems. Especially for most of us, where our job is a huge portion of our income. Some approaches to make the most of your career:

Money tip #5: Change your job

Should you change jobs? Change industries? How do you know whether to stay put or to take a risky move that will result in more money? By using the Bezos Regret Minimization Framework.

Ask yourself: Which will you regret more 20 years from now: Staying in your current situation or trying something new and failing?

And remember: the more responsibility you have, the more money you can command.

More on that here:

Deciding when to take risks in life.

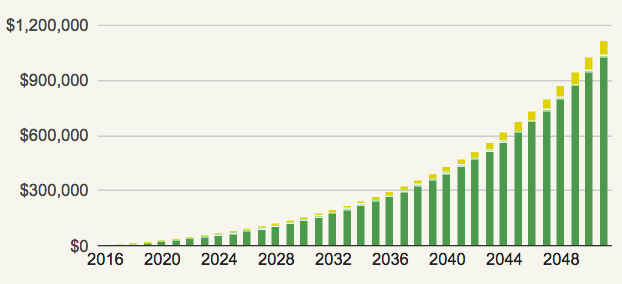

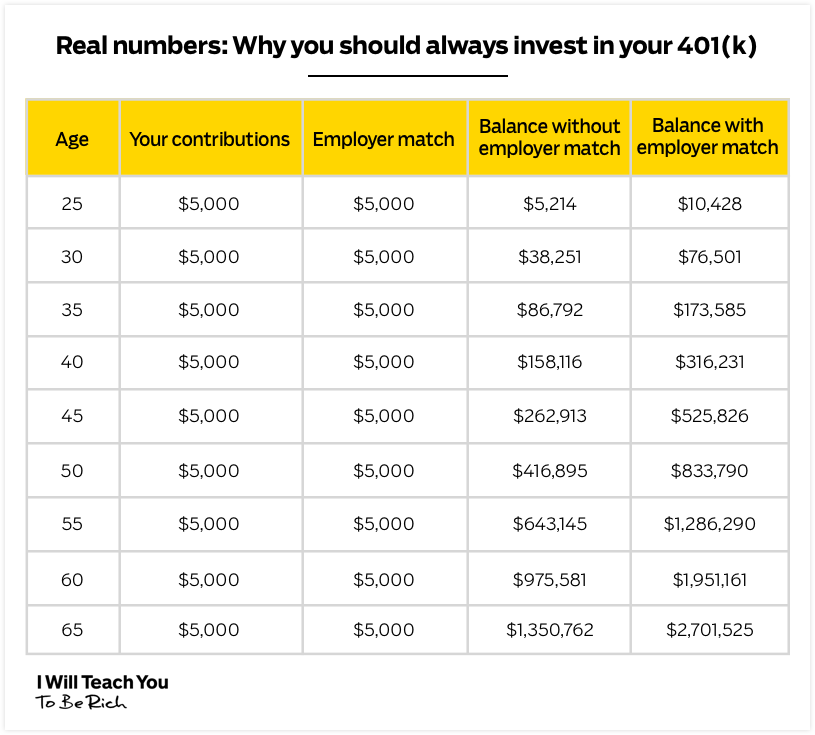

Money tip #6: Invest to earn seven figures over your life

A common chorus I hear from older people is how much they wish they got started investing earlier in their lives. That’s because investing is the most important factor determining your future financial success.

Imagine you’re 25 years old and you decide to invest $500/month in a low-cost, diversified index fund. If you do that until you’re 60, how much money do you think you’d have (assuming a 5% return)?

Take a look:

$1,116,612.89.

That’s right. You’d be a millionaire after only investing a few thousand dollars per year.

NOTE: I’m not talking about trading individual stocks, wearing a power suit with shoulder pads, and making “deals.”

Hollywood ≠ reality.

The type of investing I’m talking about is in low-cost, diversified index funds over decades.

Smart investors value consistency over anything else. Not the “hottest” stock. Or fad investments.

But this all begs the question: What should YOU invest in?

Two things:

A 401k through your employer A 401k is an investment plan offered by companies. The good ones will offer an employer match.

These investment accounts use your pre-tax income in order to invest for you. That means the money you put in will compound and grow until you can take it out at the age of 59 ½. You’ll be taxed on the money you withdraw then.

So take advantage of your employer’s 401k plan by putting at least enough money to collect the employer match into it. This basically means that for every dollar you contribute, your company will match that (pre-tax!).

This ensures you’re taking full advantage of what is essentially free money from your employer. That match is POWERFUL and can double your money over the course of your working life:

As of 2018, you can contribute up to $18,500 / year. If you can do that, be sure to give me a call because drinks are on you tonight.

Roth IRA Much like your 401k, you’re going to want to contribute as much as you can to this account. Unlike a 401k, though, you contribute after-tax income to this account.

The amount you are allowed to contribute goes up occasionally. As of 2018, you can contribute up to $5,500 each year.

I suggest putting money into an index fund such as the S&P 500 as well as an international index fund as well.

Note: If $500/month sounds like a lot, read all the ways you can free up that money with just a few phone calls.

Money tip #7: Start an online business

There’s no question that if you really want to make more money, starting an online business is one of the best ways to do it. It’s also a great way to find freedom and self-worth.

In another article, I explain how to find online business ideas, set some ground rules for starting an online business, dig into your options, and finally present the best business to start.

Money tip #8: Meet successful people who hang out with other successful people

Opportunities come through people. Ryan Holiday became the director of marketing at American Apparel … when he was only 21. How’d he do it? Not by RANDOM TACTICS but by taking a systematic approach to meeting people he admired and offering to help. Not by forcing awkward interactions, but by adding value.

Networking doesn’t have to be a scuzzy, inauthentic thing where you hand out a bunch of business cards. Instead try what I call “Natural Networking” by starting off with “informational interviews.”

First, an informational interview is an opportunity to meet someone you’re curious about and learn from them. Maybe you’re curious what a front-end programmer really does. Maybe you want to know what the culture at Google is like. That’s what an informational interview allows you to do.

Start by brainstorming 10 people you’d like to meet.

Find something in common with them. It can be you went to the same university, have common contacts, anything that separates you from the rando weirdo emails they get.

Send them an email. A script you can use is below:

To: Jane

From: Samantha

Subject: Michigan State grad — would love to chat about your work at Deloitte

Hi Jane,

My name is Samantha Kerritt. I’m a ’04 grad from Michigan State (I know you were a few years before me) and I came across your name on our alumni site. [TELL THEM HOW YOU CAME ACROSS THEIR NAME SO YOU DON’T SEEM LIKE A CREEP.]

I’d love to get your career advice for 15-20 minutes. I’m currently working at Acme Tech Company, but many of my friends work in consulting and each time they tell me how much they love their job, I get more interested. [THE FIRST SENTENCE SAYS WHAT SHE WANTS. MOST PEOPLE ARE FLATTERED THAT PEOPLE WANT/VALUE THEIR ADVICE.]

Most of them have told me that if I’m interested in consulting, I have to talk to someone at Deloitte. Do you think I could pick your brain on your job and what motivated you to choose Deloitte? I’d especially love to know how you made your choices after graduating from Michigan State. [THE PHRASE “PICK YOUR BRAIN” IS ONE OF THE BEST WAYS TO ASK FOR ADVICE AND FLATTER, AND “MICHIGAN STATE” REINFORCES SHARED BOND.]

I can meet you for coffee or at your office … or wherever it’s convenient. I can work around you! [THE BUSY PERSON IS MORE IMPORTANT THAN YOU. TREAT THEM ACCORDINGLY.]

Would it be possible for us to meet? [A BUSY PERSON CAN SIMPLY REPLY TO THIS WITH A “YES” — PERFECT. NOTE THAT I DIDN’T ASK FOR THE TIME/LOCATION AS THAT’S TOO MUCH INFORMATION IN THE FIRST EMAIL.]

Thanks,

-Samantha

The single best way to earn money

Most people will focus on the little things. Not you — if you do the above you will be ahead of 95% of your peers. Everything above is a repeatable SYSTEM and not a one-and-done tactic.

With that in mind, I put together a special bonus for you.

In this 11-minute video, I’ll show you how you can create the perfect system to automatically take care of your money every month.

This is the single best way to earn money, save money, and invest money into your Rich Life.

No more panicking if you have enough in your checking account to pay the bills — it’s my gift to you. This system took me 10 years to perfect and it’s being used by thousands of my students successfully.

The following is a guest post by Moss Mint Teal, which explores the intersections of sustainability and personal finance while examining the impacts of systemic issues like discrimination on the basis of race, gender, and more. What the term “personal finance” is missing We often hear how “personal finance is personal,” but what about when [...]

Some common themes I see are fear, laziness, confusion, and even anger.

If that sounds familiar to you, that’s okay! I want to be there to help.

That’s why we’re going to break it down to the basics today: Budgeting 101.

The problem with your budget

When people think budgeting, images of their parents studiously going over receipts, writing down expenses in a notebook, and screaming, “HOW DID WE SPEND SO MUCH ON GAS LAST WEEK?” come to mind.

That might have worked for them … but it sure doesn’t work now.

How many times have you opened your bills, winced, then shrugged and said, “I guess I spent that much”?

How often do you feel guilty about buying something — but then do it anyway?

This is unconscious spending (aka “spreadsheet budgeting”). The main issue with it is simple: Human willpower.

Who wants to track their spending? The few people who actually try it find that their budgets completely fail after two days because tracking every penny is overwhelming.

3 alternative budget help tips

Instead, we’re going to gently create a new, simple way of spending.

I’m going to help you redirect it to the places you choose, like investing, saving, and even spending more on the things you love (but less on the things you don’t).

This is going to be the foundation of your Conscious Spending Plan.

Budget help #1: Automated finances

Let’s get on with the specifics of how you can make your own Conscious Spending Plan. I’m not going to lie to you: It’s difficult and requires a bit of time on your part. But I’ll try to make it as painless as possible.

Take heart in the fact that this isn’t an overly complex system. All you need is to just get a simple version ready today and work to improve it over time.

A Conscious Spending Plan involves four major buckets where your money will go:

Fixed costs (e.g., cell phone, rent, utilities)

Investments (e.g., 401k, Roth IRA)

Savings (e.g., vacation, wedding, house down payment)

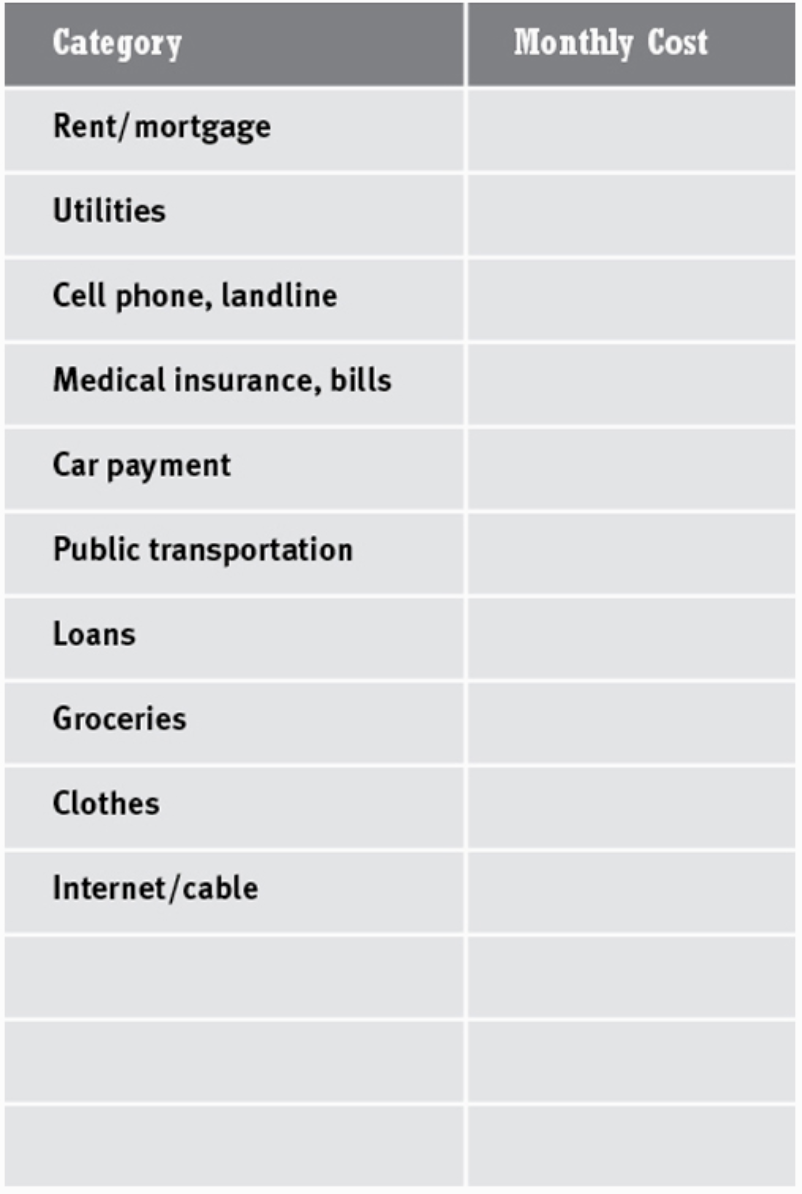

Fixed costs These are things you absolutely need to pay every month such as your rent, utilities, student loans, mortgages, and cell phone.

It’s important you figure out this number first as this is money that’s going towards your essentials. Everything else you can change. This is fixed.

Here’s a chart with some common expenses any ordinary person would use to live. If you see any glaring omissions, add them.

Monthly fixed costs

Create your own version and fill in how much you spend on it each month.

If there are any you haven’t accounted for, you’ll need to go through your bank statements and see how much you spent on those categories in the past.

Remember: You don’t have to be incredibly precise here. As long as you get close, it’ll be good enough.

Once you’ve done that, I want you to add 15% onto each amount. This helps you cover for things you haven’t figured in. Don’t worry if this seems like too much. As time goes on, your system will get more and more precise.

When you have a total number for your fixed monthly costs, subtract it from your monthly take home pay. Now you know exactly how much you have to spend on other categories.

Plan to spend around 50% – 60% of your income on this bucket.

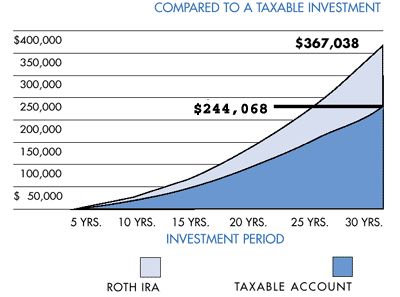

Investments At a bare minimum, this category should cover your 401k and Roth IRA.

Check out this simple graph on how much you stand to earn when you invest in a Roth IRA vs a taxable account.

That’s a difference of $122,970!

You’ll want to put away as much money as possible into these accounts. So plan to invest at least 5% of your income after taxes.

Don’t know how much you should be investing? Check out this retirement calculator. It’s one of my favorites and can give you a great idea on how much you should be saving in order to retire.

Savings This is for any money goals you might have. They could be:

Short term. Think Christmas gifts, vacations, or that sweet new pair of Yeezys you’ve been eyeing.

Long term. Very big purchases such as a down payment on a house, or your child’s college degree.

One of my favorite ways to save is with sub-savings accounts. These are accounts you create to save for specific purchases or events.

My old sub-savings accounts.

This is precisely how people accomplish financial goals passively. Because when you don’t see the money — when it’s automatically withdrawn from your checking account and funneled to specific savings goals — you will never miss it. However, a few months later, you’ll be amazed at how quickly you’re progressing to your targets.

Guilt-free spending Ahh this is my favorite part of the automated finances system. After putting your house in order, and allocating money for investing, saving, and fixed costs, you’re now ready to spend it on the things you love.

This includes things like restaurants, bars, Uber/Lyft rides, movies, shopping, and weekend trips.

This is going to be 20% – 30% of your take home pay. A little later, I’m going to show you exactly how you can spend money on all the things you love without worrying about it. But first, you need to learn how to set up your system.

ACTION STEP: Set up your system in one weekend.

Set aside a few hours this weekend. What you’re going to do is go to your bank’s website, and set it up so the money is automatically transferred to the above four buckets each month. This might also take a few phone calls so be ready.

Make sure you have the numbers in front of you to streamline the process.

If you need more information on how to do all this, be sure to check out my 12-minute video below, where I break down exactly how automated finances work.

Budget help #2: Spend on what you love (and only that)

To make sure you’re really being conscious about your spending, you need to spend on the things you love — while ignoring everything else.

That’s right: I’m telling you to SPEND money in an article about budgeting.

To do that, I’m going to tell you the story of two friends of mine. At first glance, they couldn’t seem more different, but if you look closely you’ll see that they’re both spending on what they truly love and living a Rich Life because of it.

Conscious Spending case study #1: She spends $5,000 / year on shoes I have a friend who LOVES shoes.

Not just any shoes either. I’m talking about high-end footwear that costs at least $300 a pair.

Oh, and she buys about 15 pairs each year.

I can hear some of you screaming now, “WTF THAT’S ABSURD! WHAT A WASTE OF MONEY!”

On the surface, that does seem like a lot. But what you don’t know is she makes a healthy six-figure salary, has a roommate, and eats for free because of work.

Her 401k and other investment accounts are fully funded. She’s also saving her money for all of her savings goals like vacations.

On top of that she’s ruthless about cutting out the things she doesn’t care about. That means avoiding new tech gadgets, gym memberships, or eating out. She also lives in a tiny room in a small apartment because she doesn’t care about having a fancy place.

After planning for her long-term and short-term goals, she has money left over on the thing she does care about: Her shoes.

Conscious Spending case study #2: The non-profit worker

And you don’t have to be making more than six figures to live a Rich Life.

I had a friend who worked at a nonprofit in San Francisco. She was making about $40,000 / year — but was saving $6,000 / year …

… IN SAN FRANCISCO.

How does she do it? Simple: She’s conscious of her spending.

She cooks at home, shares rent in a small apartment, and is reimbursed for her driving by her office.

When she’s invited out to eat, she checks to see if she can afford it. If not, she politely declines. But when she does go out, she never feels guilty about spending because she knows she can afford it. Yet it’s not enough to save money on just rent and food. She also chooses to save aggressively, maxing out her Roth IRA and putting aside extra money for traveling. Each month, that money is the first to be automatically transferred out.

Talking to her, you would never know that she saves more than most Americans. But in reality, she’s chosen to put her investing and saving priorities first.

ACTION STEP: Be conscious about your spending.

To help you with that, I suggest the Envelope System. This is a system of making sure you have money for things like going out and shopping each month. For more on the system, check out my article on how to save cash.

Budget help #3: Free up your money

The best way to ensure flexibility in your budget is to earn more money.

And there are a few different ways you can do this:

Negotiate a raise. If you have a job, this is a no-brainer … but it takes a lot of planning and study. Be sure to check out my article on salary negotiations for more.

Tap into hidden income. With a few 5-minute phone calls you can save yourself THOUSANDS every year. Find out how with this free PDF.

Do freelance work. Starting a side hustle is one of my favorite ways to make money. Using the skills you already have, you can start fuel-injecting your income. Here’s how to find the best side hustle ideas today.

If you apply the right systems you can find the money to make expensive purchases AND earn money at the same time.

That’s why I want to offer you something:

The Ultimate Guide to Making Money

In it, I’ve included my best strategies to:

Create multiple income streams so you always have a consistent source of revenue.

Start your own business and escape the 9-to-5 for good.

Increase your income by thousands of dollars a year through side hustles like freelancing.

Download a FREE copy of the Ultimate Guide today by entering your name and email below — and start earning more money today.

EQ Bank is a digital bank that has been around for a few years but I only just started using in January. I waited too long! In this EQ Bank review I share what’s to love (and some things not to like) about this newcomer to Canadian banking. A 100% honest EQ Bank review Many [...]

Earning six figures a year can be the finish line.

It can be the golden milestone, the badge of honor showing to the world that you made it and have now claimed your fat slice of the American Dream.

You can save more. Invest more. And most importantly, spend more. Once you start earning six figures, you’re a “high earner.” You get the velvet rope treatment and enter a club with other high earners basking in your newfound echelon of society.

Well, that used to be true. What was unimaginable before is becoming increasingly common: Some people need much, much more than $100,000 a year to get by.

High earners in the most expensive cities in America

The internet lost its collective mind in July 2018 when the U.S. Department of Housing discovered that a family of four living on an income of $117,400 would be considered “low income” in San Francisco.

Of course, at first glance this sounds ludicrous. Six figures is the gold standard of high-earning. How is it possible that you’d be considered “low income” when you’re earning more than $100,000 a year?

“I live in the D.C. area, so $100,000 doesn’t make anyone’s jaw drop,” says Steve, 41. “If you’re making $200,000, that’s good but it’s still just upper-middle class around here.”

Like many in the area, Steve (not his real name: several names throughout this piece have been changed) is a contractor for the federal government earning roughly $200,000 a year. He’s also very familiar with the high income needed to sustain living around our nation’s capital, which is home to the richest county in the nation.

“I once did a cost of living analysis of D.C. and found that it was comparable to some of the most expensive cities in America,” he says.

And he’s right. Washington, D.C., stands toe-to-toe with the likes of Manhattan, New York; San Francisco, California; and Los Angeles, California, as one of the the most expensive cities to live in.

Nearly 3,000 miles away in the shade of the San Gabriel mountains, Marc, 47, knows the feeling too. He lives with his wife and two sons in Burbank, California, just north of Los Angeles.

While his job as a freelance television editor provides him with roughly $175,000 a year, he also feels the constraints of the city he lives in.

“Housing is pretty ridiculous in LA,” Marc says. “We bought our house in Burbank in 2009 at the height of the housing market crash. Even then it was still pretty expensive.”

A recent report by CoreLogic, a real estate analytics firm, found that home prices in Los Angeles are actually grossly overvalued. In fact, housing prices are 10% above where they should be with long-term trends.

The result: Home costs in LA are outpacing the consumer’s ability to purchase them.

Marc sometimes struggles with a high mortgage. As an independent contractor, he goes through frequent periods of feast or famine. Depending on the season, he might not get work for a while.

“Over the past year, I’ve had three weeks where I just didn’t have work,” he says. “It’s a little bit of a hustle. Finding work can be a pretty consistent thing, but maybe it’s because I have a family to support and a mortgage. I feel pressure to keep the machine running.”

That pressure can follow you even in the best of times too.

Debra lives out of Staten Island with her husband and two-year-old son, and works in New York as a business consultant earning a base of $135,000 a year. But that wasn’t always the case. In fact, she lived for a decade abroad in Israel earning a fourth of what she does now.

“I’ve always been very ambitious,” says fellow high earner Debra, 34. “So whatever I’m making, I always want to make more. On the one hand, though, I’m making six figures, which is considered the gold standard for high earning.”

Living in the NYC area comes with its own challenges though. Finding affordable housing in the city is so difficult it’s spawned memes, YouTube vids, and even a Tumblr blog dedicated to terrible and expensive New York apartments.

That hasn’t stopped Debra from starting a family in nearby Staten Island though.

“The fact that I’ve broken through [to six figures] is exciting,” she says. “Financial institutions think so too since I recently got approved for a mortgage.”

She has high hopes for her future and building out her version of a Rich Life — and her income helps with that dramatically. But still, even she’s a little nervous about the future.

“I’m the main breadwinner right now,” she says. “So I’m in the position where I’m trying to keep my family afloat. It adds a lot to stress.”

She continues, “I remember a few months ago, my family was renting in an apartment that turned out to be infested with mice. It was terrible. If I were single, I’d just go sleep on someone’s couch. No big deal. But since I had a family, we were essentially facing homelessness. I felt on the verge of a breakdown.

“When you’re faced with the tremendous pressure of needing to have a job at all times, you start thinking, ‘What do we REALLY need to get by?’”

And in all likelihood, it’s more than the six-figure salary she is earning now.

“It’s a lot of pressure,” she says.

The belt tightens at $175k

In LA, finances are often top of mind for Marc for three reasons:

1. The sporadic nature of his freelance video editing job.

2. His family he must provide for.

3. His mortgage, which he must pay if he wants to keep his house.

Since work can be uncertain as a freelancer, he’s turned to “diversifying” his earnings through Airbnb side hustles.

Still, when finances get short, he really starts to feel it.

“We do have to tighten our belt during lean periods,” he says. “We have to cut out contributing to our retirement and kids’ college funds. I’m 20 years out from retirement, so when there’s a year we don’t contribute the full amount to our Roth IRAs, it’s a lot of money. It’s really not the place I want to be.”

He continues, “I hate it sometimes. I absolutely hate it. Don’t get me wrong: I love my job. I love my family. I love my life here. But since I’m the financial person and breadwinner in my family, I feel that burden resting squarely on my shoulders.”

Delaney and the theory of relativity

Just a few hours south of San Francisco (home of the low-income six-figure family) lives Delaney, 52.

She lives in a small nondescript California city of 40,000 people. There the cost of living is very low — or at least it is when compared to LA and San Francisco.

Looking at her life, you wouldn’t think she’s a high earner. Unmarried and with no children, she lives in a small three-bedroom house amongst a neighborhood of others. She drives an old Fiat. For fun, she likes to play the guitar and go camping with friends.

However, she’s actually a web developer who makes more than $11,000 a month as a freelancer.

Despite this, she’s apprehensive to say that she’s a high earner.

“Relative to my community, I’m a high earner,” Delaney clarifies. “But if I lived in San Francisco, I’d be barely getting by. If I lived in New York, I’d be barely getting by. In my little bitty niche of the world, though, I’m definitely a high earner. I earn well over twice the median for my community.”

She continues, “It’s all relative though.”

And she’s right. The people we spoke to earned roughly the same salary — yet experienced completely different perspectives on what it meant to be a high earner.

While some felt like their income was just barely enough some days to get by (like with Marc and sacrificing his retirement fund), others were more than happy with what they had (like Delaney).

Earning six figures is an awesome thing to aspire to. And, depending on where you are, it can give you a great living and allow you to live out your Rich Life.