I’m a big fan of online banking services or credit unions over Big Banks (e.g., Bank of America, Wells Fargo, the banks that Satan uses). Avoiding the big guys typically gives you access to the best checking accounts with great rewards and almost no downsides.

Most importantly: online banks and credit unions don’t try to nickel-and-dime you with fee after fee.

I’ve studied most of the checking accounts on the market, and today, I’ll show you the best one I’ve found. In fact, it’s the one I use as my primary checking account.

Charles Schwab Investor Checking: The best checking account

Most people think of Charles Schwab as a bank solely focused on investments. But they also offer what I believe to be the best checking account available. Why?

No fees

No minimums

No-fee overdraft protection

Free checks

Deposit checks via pre-paid envelopes or via iPhone app (snap photos of your check — no need to go into branch)

An ATM card

BEST BENEFIT: Unlimited reimbursement of any ATM usage

This last point is what puts Schwab over the top. How often do you go out with friends and have to withdraw money from out-of-network ATMs? How often do you find yourself at a cash-only taco place at 3:30am, needing to withdraw $280, but you hesitate because of onerous ATM fees?

Me too.

Those fees can add up, and Schwab reimburses you for all of them. If you rack up $200 worth of ATM fees in a month, you’ll see a $200 deposit from Schwab before the month ends. This means you can use ANY ATM — corner stores, other banks, whatever — without having to look for some specific bank’s ATM.

Some people will balk at using Schwab because it’s an online bank. That’s fine, but I urge you to reconsider: It’s rare to find a checking account that (1) avoids screwing you at every turn, and (2) actually rewards you for using them.

You know by now that I’m all about Big Wins. This perk alone can result in hundreds of dollars a year that you do nothing to redeem. The ATM-fee reimbursement for the rest of your life is enough of a benefit, but stack on the trust Schwab has built with me, and I’m a long-term customer.

How to open a Charles Schwab checking account

To get started with the Schwab Checking Account, click here. Note: It’s not an affiliate link. I have no relationship with Schwab except being a happy customer.

To learn how to fully automate your finances — including ultra-specific recommendations on accounts, investing, debt, negotiation, money & relationships, and buying a car/house — pick up a copy of my book, on sale for less than $10.

Honorable mentions

I LOVE my Charles Schwab checking account. I think it’s the best checking account out there — but I also know there are a ton of other great ones out there too.

Here my other three suggestions for fantastic checking accounts:

Your local credit union

Credit unions are like local banks, but they’re not-for-profit and are owned by their customers (or, in credit union parlance, “members”).

As a result, credit unions usually provide better loan rates and more personalized service than other brick-and-mortar banks. So I’m a BIG fan of them.

Most will allow you to establish a checking account, savings account, or loan, although some require membership in associations like any other unions.

Full disclosure: I’ve spoken at a number of their national conferences to help them understand how to reach young people, which I loved doing because I hope they succeed in reaching out to other twentysomethings.

To find a credit union near you go to this link and enter in your information.

Capital One 360 Checking

Long-time readers know that I was a HUGE fan of ING Direct Electric Orange account before they merged with Capital One and became Capital One 360.

While a lot of people were worried (i.e., freaking terrified) that Capital One would get rid of all of the things we loved about ING Direct, the checking account is still actually a pretty good deal.

A few things I LOVE about this account:

No fees

No minimum

Free ATM access to over 38,000 Capital One ATMs

Automatic overdraft protection

The only reason I don’t use this account for checking is because it doesn’t offer free ATM withdrawals (like Charles Schwab checking). Still a fantastic option though.

Ally Interest Checking

Another checking account I love is Ally Interest Checking. Ally is an online bank, meaning there are no physical locations, eliminating overhead and allowing them to offer dramatically higher interest rates than traditional Big Banks.

A few reasons Ally is great:

No monthly fee

No minimum

24/7 banking staff

Access to over 43,000 ATMs

0.10% APY (That goes up to 0.60% if you have at least $15,000 balance)

Up to $10 in ATM fees reimbursed per statement cycle

Ally is an all-around fantastic online bank.

“The Inbox:” Why you need the best checking account

Choosing a checking account that works for you is crucial because it’s at the center of your personal finances.

I write often about building an automated personal finance infrastructure — a system that funnels your money to where it needs to go on a schedule, with minimal involvement from you.

This way, the money left over after bills is yours to spend guilt-free. Chapter five of my book is all about how this system works and how to build your own.

Of all the components in that system, none are more crucial than your checking account. As I wrote in the book:

“I think of my checking account like an e-mail inbox: all my money goes in my checking account, and then I regularly filter it out to appropriate accounts, like savings and investing, using automatic transfers.”

Your checking account is the center of it all, the nexus of your bulletproof personal finance system. Unfortunately, as I also point out in the book, checking accounts are the number one place where unnecessary fees are levied.

That’s why I want to go into what exactly you should be looking for when searching for checking accounts — even if you DO choose the ones I recommended above.

3 things to look for in checking accounts

I look for three things when it comes to deciding whether or not a bank has a good checking account: trust, convenience, and features.

1. Trust

For years, I had a Wells Fargo account because their ATMs are convenient, but I don’t trust Big Banks anymore.

I’m not the only one. At the moment, Big Banks are looking around wildly, wondering why young people like me are moving to high-interest accounts online.

Perhaps it’s because they secretly insert fees, like the filthy double charges for using another ATM, then count on our inaction to make money off us.

Perhaps it’s because they like to nickel-and-dime you every step of the way.

Perhaps it’s because they’re evil incarnate, forged in the hell fires of damnation where mercy, hope, and happiness doth not shine—

Okay. I MIGHT have a bit of a chip on my shoulder when it comes to Big Banks.

There are still some good banks out there, though. The best way to find one is to ask friends if they have a bank they love.

Your bank shouldn’t nickel-and-dime you through minimums and fees. It should have a website with clear descriptions of different services, an easy setup process, and 24/7 customer service available by phone.

Another thing: Ask them if they send you promotional material every damn week. I don’t want more junk mail! Stop sending crap! A couple of years ago, I switched my car insurance because they would not stop sending me mail three times a week. Go to hell, 21st Century Insurance.

2. Convenience

If your bank isn’t convenient, it doesn’t matter how much interest you’re earning — you’re not going to use it.

Browse the bank’s website. See what features they have.

Since a bank is the first line of defense in managing your money, it needs to be easy to put money in, get money out, and transfer money around. This means its website has to work, and you need to be able to get help when you need it — whether by e-mail or phone.

3. Features

The bank’s interest rate should be competitive. If it’s an online bank, it should offer value-added services like prepaid envelopes for depositing money and convenient customer service. Transferring money around should be easy and free because you’ll be doing a lot of it, and you should have free bill paying. It’s nice if the bank lets you categorize your spending and get images of canceled checks, but these aren’t necessary.

5 ways banks try to trick you

While you’re searching around, also keep an eye out for ways a bank is trying to trick you.

Banks LOVE to pull scammy marketing tricks to get you to buy into their services. Luckily I’m here to show you exactly what they’ll try to do — and how you can avoid it.

Teaser rates like “6% for the first two months!” Your first two months don’t matter. You want to pick a good bank that you can stick with for years — one that offers overall great service, not a promo rate that will earn you only $25 (or, more likely, $3). Banks that offer teaser rates are, by definition, to be avoided.

Requiring minimum balances to get “free” services like checking and bill paying.

Up-sells to expensive accounts (“Expedited customer service! Wow!”). Most of these “value-added accounts” are designed to charge you for worthless services.

Holding out by telling you that the no-fee, no-minimum accounts aren’t available anymore. They are. Banks will resist giving you a no-fee, no-minimum account at first, but if you’re firm, they’ll give you the account you want. If they don’t, threaten to go to another bank. If they still don’t, walk out and find one that will. There are many, many choices and it’s a buyer’s market.

Bundling a credit card with your bank account. If you didn’t walk in specifically wanting the bank credit card, don’t get it.

By recognizing these tricks, you’ll be able to find a checking account that works for you while avoiding all the scams.

Automate your checking account

Want to learn the system I use to get more out of my checking account — and spend just minutes a week on your finances?

I have the perfect system for you:

Automating your personal finances

I mentioned it above — but if you don’t know what it is, prepare to be blown away at how effortless saving and investing can be.

I’ve created a 12-minute video showing you exactly how this system works. Just enter your information below and receive it in your inbox for FREE.

An emergency fund gives you a financial cushion for unexpected expenses.

What would happen if your car gets totaled in a crash?

Or you or a loved one gets sick or injured?

Or you’re fired from your job?

Okay I’ll stop trying to give you an anxiety attack. The point is you need to have money to provide for those moments.

People often don’t factor in unexpected purchases into their financial plan. Nobody ever expects their car to break down or for them to fall seriously ill.

Most Americans wouldn’t be able to cover a $500 surprise expense. So if you are one of the four in ten people who do have an emergency fund, you’re ahead of the majority of people AND you’re better positioned for unexpected purchases.

If you don’t have the cash, don’t worry. You’ve come to the right place. I’m going to give you a system to create an emergency fund passively AND show you when exactly to use the money.

An emergency fund is money saved for any unexpected expenses. The actual amount varies from person to person — but it should contain enough money for three to six months of living expenses.

More importantly, though, it gives you the peace of mind knowing you have a hedge against the worst financial disasters AND allows you to be more aggressive in other areas of your life (e.g., investing, starting a side hustle).

There are two situations where you’ll be glad you have that emergency fund:

Surprise expenses

Loss of income

Let’s walk through each to see what they might look like.

Unexpected expenses

Did you know that 10% of Americans took a “hardship withdrawal” from their 401k in 2015?

That means they had to withdraw money from their retirement fund, incur a hefty penalty for it, and slow their retirement plans because they didn’t have money for emergencies.

Think about that: 10% of Americans had to put off their retirement goals because they did not have an emergency fund. Your 401k and other retirement accounts should be money saved for your financial future — not to be used for unexpected expenses like:

Medical bills

Financial/identity theft

Car repairs

Home repairs

Economy crashes

Let’s be honest: You can’t always choose whether to dip into things like credit cards or your retirement during emergencies — and that’s okay! As the wise proverb goes: Shit happens.

BUT you can anticipate the unexpected by starting an emergency fund today. Doing so will soften the impact of major financial emergencies you may encounter.

Loss of income

No one ever “plans” to lose their jobs BUT it happens. If it does happen to you, you need to be able to support yourself and your loved ones.

That’s why I recommend you have three to six months of living expenses in the bank for these situations.

The average duration for unemployment in the U.S. is just a little more than five months (per Bureau of Labor Statistics). I have six months of cash for this very reason. I know. I know. I’m the CEO of a personal finance company, how could anything go wrong? *knocks on wood*

This money provides me with peace of mind because I know I’ll be able to withstand the pressure if I ever need to use it.

How to start an emergency fund

Putting money towards an emergency fund is an AWESOME goal to have. But let’s be candid, it might take a while depending on how much you can put away each month.

For instance, if your expenses are $1,000 a month and you can only put away $50 a month towards your emergency fund, it’s going to take you ten years to save enough to have six months in the bank.

There’s one thing I want you to know: That’s okay! 57% of Americans have less than $1,000 in their savings account. That means if you save anything at all, you’re putting yourself in a better financial position than the vast majority of people.

Your emergency fund is going to take a long time to build. That’s why I’m going to show you how to build your emergency fund AND earn more money so you can finish your goal sooner. There are four steps to get there.

Step 1: Find out how much you need

First we need to know how much you need in your emergency fund.

To do that, you have to add up three to six months’ worth of:

Basically, any living expense that you have should be accounted for. Add them all up and you’ll have a rough estimate of how much you need. It’s okay if it’s not perfect. A ballpark figure will work.

Here’s a quick table that’ll show you how much you’ll need based on potential expenses:

MONTHLY EXPENSES

EMERGENCY FUND (3 – 6 MONTHS)

$500

$1,500 – $3,000

$1,000

$3,000 – $6,000

$2,000

$6,000 – $12,000

$3,000

$9,000 – $18,000

$4,000

$12,000 – $24,000

$5,000

$15,000 – $30,000

The average yearly expenses for Americans total $57,311 — or about $4,776 a month. So that means you should save about $14,328 to $28,656.

TIP: If your goal was to save up $14,328 and you were putting away $500 a month towards your goal, it’d take over two years to get there. Like I said, this is going to take a while — but I’ll show you how you can start saving easily with a great system.

When it comes time to use your emergency fund, you’re likely going to have to make some sacrifices, ESPECIALLY if you just lost your job.

This means you might have to cancel things like cable, Netflix, Uber/Lyft rides, gym memberships, and that recurring reservation at your favorite caviar fried chicken place.

“But Ramit! That goes entirely against your Rich Life philosophy! Why shouldn’t I be able to buy a latte with my emergency fund?”

Listen, there’s nothing stopping you from using your emergency money while living the lifestyle you want. You just have to factor that into your savings goals.

At the end of the day, this is your emergency fund. You can put as little or as much in it as you want. Just know that this money is there to get you through some of the toughest financial disasters of your life.

Maybe you’re content living at 70% of your current expense. Maybe nothing less than 100% is acceptable. Either works, just put away your money accordingly. When those moments happen, sacrifice might very well become necessary.

Once you know how much you roughly need to get you through three to six months, it’s time to open an account where your money will live.

Step 2: Open an account

There are two places you can put your emergency fund:

A checking account

A savings account

There are pros and cons to each. If your money is in a checking account, it can be more readily available for when emergencies happen. However, it can also be much easier to dip into your emergency fund for NON-emergencies because of your limited willpower.

You might prefer then to put your emergency fund in a high-yield savings account. There it can safely sit until your rainy day (and the government will insure your cash up to $250,000).

One suggestion: Find a bank that allows you to have a sub-savings account too.

This is an account you open along with your regular savings/checking accounts that can be used for specific expenses. Chances are your bank already does this. If your bank doesn’t, that’s okay! You just need to find one that does.

Here are a few great suggestions for banks that offer great savings accounts (with sub-savings):

Your bank might even allow you to give the account a nickname. This lets your sub-savings accounts reflect your savings goals.

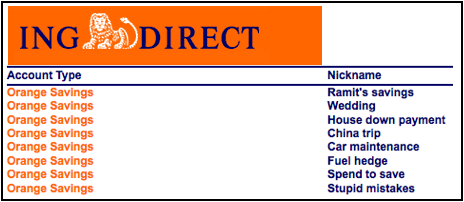

Check out all the different sub-savings accounts I had in my old savings account.

ING Direct is now Capital One 360. BTW that wedding one is going to be put to good use.

Here’s a look at a few sub-savings accounts I have now:

ING switched to Capital One 360, and I used the money I saved to buy an engagement ring

So create one and name it “Emergency Fund.” Once you have your account, it’s time to start putting away money using an automated system.

Step 3: Automate your emergency fund

Automated finances are the ultimate cure to never knowing how much you have in your checking account and how much you can spend.

When you receive your paycheck, your money is funneled to exactly where it needs to go.

Check out my video below to learn exactly how to set it up today.

I recommend you automate your accounts so you’re sending around 5% of your income into your emergency fund.

Knowing how much you’re putting in each month also lets you know exactly when you’ll hit your goal — allowing you to rest easy knowing your personal finance machine is working for you.

The hard cash amount might change as you get raises, change jobs, or come into extra money. That’s fine! The important thing is that you’re saving even if it’s a small amount.

Step 4: Earn more for any emergency

Earning money for your emergency fund is going to take time. The length of time it takes depends entirely on how much you’re earning and how much you want to put away.

If you want to put away more and crush your savings goals sooner, there’s one great way to do it: Earning more money.

That’s why my team and I have worked hard to create a guide to help you earn more today:

The Ultimate Guide to Making Money

In it, I’ve included my best strategies to:

Create multiple income streams so you always have a consistent source of revenue.

Start your own business and escape the 9-to-5 for good.

Increase your income by thousands of dollars a year through side hustles like freelancing.

Download a FREE copy of the Ultimate Guide today by entering your name and email below — and start earning more for your emergency fund today.

For many people, just the words “tax season” bring on financial stress and headache, but filing your taxes has never been easier. Before we jump into it, I want to invite you to join me and H&R Block Canada tax professionals for a Tweet Chat tomorrow! #GetWhatsYours H&R Block Canada Tweet Chat Tuesday March 27, 2018 @ 6pm CST / 7pm EST Follow @moneyaftergrad + @HRBlockCanada Over $700 in prizes! While I hire an accountant to manage my business financials, I’ve always taken care of filing my personal income taxes myself. While initially intimidating, once I became familiar with the process and the paperwork, filing my own taxes became quick, easy, and saved me hundreds of dollars every tax season. Now that Canada Revenue Agency (CRA) is moving more and more towards digital records, filing your own taxes is easier than ever. Furthermore, choosing the right software helps you avoid […]

Basically, the inflation rate lessons the purchasing power of each dollar you own by an average of 3.7% each year. It’s the reason candy bars used to cost $0.50 cents and now they are $1, and the reason that keeping your money under your mattress is a bad idea (more on that below).

If you want to find out why exactly that is and how to protect your money against the dreaded inflation rate, stay close. Keep quiet. And whatever you do, don’t get separated from the group.

Inflation is the price increase of purchased products over time. This happens in countries as the purchasing power of their currency decreases.

Imagine you’re paying $1,000 a month for your apartment. Over the next year, there’s an inflation rate of 5%. Just for the sake of argument, this means that to maintain the same purchasing power — assuming your landlord is perfectly rational and there are no other variables at play — your landlord would account for that in next year’s rent by increasing it to $1,050.

Why does inflation happen? There are actually a lot of different reasons it can occur:

When supply decreases and demand increases. You know how your Uber price surges when more people in your area try to use it at one time? That’s a good example of supply/demand inflation. When more people want a product/service but there’s a small amount of that product/service, inflation occurs.

When production cost increases. When the cost to produce a product/service increases, supply decreases. This happened in the 1970s when the cost of oil increased, which affected the production process of any industry that used oil to transport their goods. Which was a LOT of different industries. Those industries reacted by increasing the price of their products, resulting in inflation.

When too much money is printed. The most famous example of this happened in post-WWII Germany when the country began to print enormous amounts of money to pay back war reparations. It got so bad that some German families literally burned cash for warmth because it was cheaper than firewood.

Bottom line: Inflation happens when the price of products increase. Though it can get out of hand as “hyperinflation,” like in post-WWII Germany or Zimbabwe in the 2000s, inflation is also a very typical occurrence for any national economy.

Zimbabwe had to print a one hundred trillion–dollar note to keep up with hyperinflation

Inflation: The silent killer

Inflation can be scary. Hell, when we look at how it has impacted countries like Germany, Zimbabwe, or Hungary, inflation can be downright terrifying.

You right now.

But inflation isn’t that bad. Economist John Maynard Keynes (you know, of Keynesian economics) even suggested that a small amount of inflation was the sign of a thriving economy.

However, inflation can be bad for individuals though — particularly, when you just keep your money sitting in a bank account and do nothing else with it.

I often hear people say things like, “I’m afraid of losing money,” as an excuse for not investing. That’s fair. After the 2008 financial crisis, many people got shaken by the effect it had on their finances.

However, you need to take a long-term view of your personal finances. You can choose among different investment options that allow you to make money despite events like recessions.

And because of inflation, you’re actually losing money every day your money is sitting in your bank account.

For example, Big Banks (Wells Fargo, Bank of America, etc.) pay about 0.01% interest on savings accounts in 2018. This means that if you put $1,000 in a savings account, you’d earn a whopping $0.10 per year. I find more than $0.10 in pennies on my way to the bathroom each morning, so I’m not very impressed by that kind of return.

So if your money were sitting in one of these Big Banks, you’d actually be losing money every day because inflation is 3%. So, you MAY be earning .01% interest on your savings account but you’re essentially losing 3% every year in terms of real purchasing power.

And yet, many people still opt to keep their money in a bank account or in their mattresses instead of putting it to work for them.

I won’t let that happen to you. In fact, I’m going to show you a few things you can do with your money today rather than let your finances get murdered by the average inflation rate.

What can you do about the average inflation rate?

While it is a good idea to have some cash on hand for things like your emergency fund, your money should be put to work through investing.

Investing is the single most effective way to get rich. By opening an investment account, you give yourself access to the biggest money making vehicle in the world: the stock market.

What should you be investing in though — and how? To answer that, you simply have to have your Ladder of Personal Finance handy.

No, it’s not something you can buy at Home Depot. The Ladder of Personal Finance takes a look at three essential areas you should be investing your money towards:

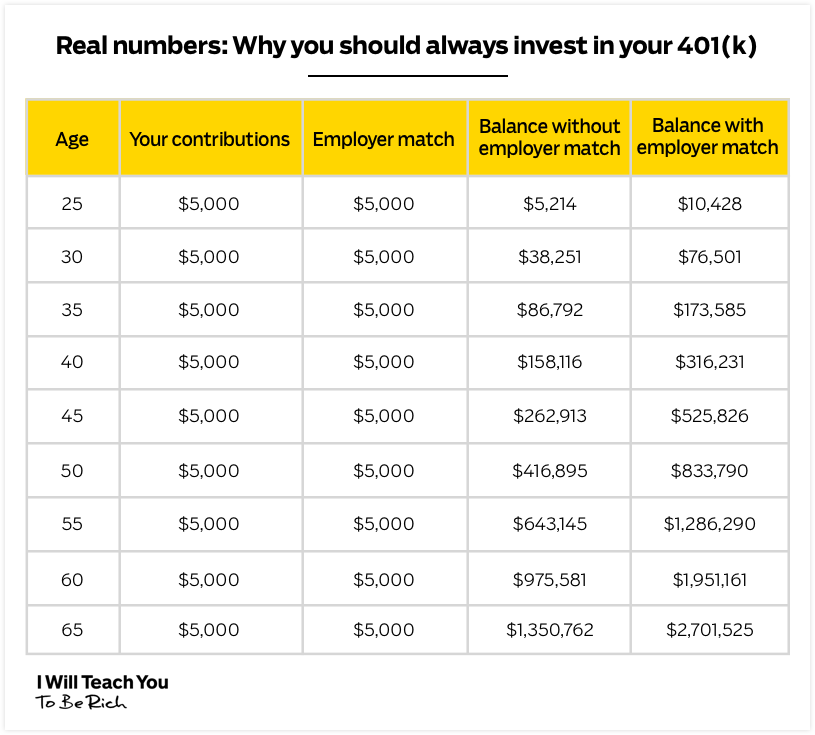

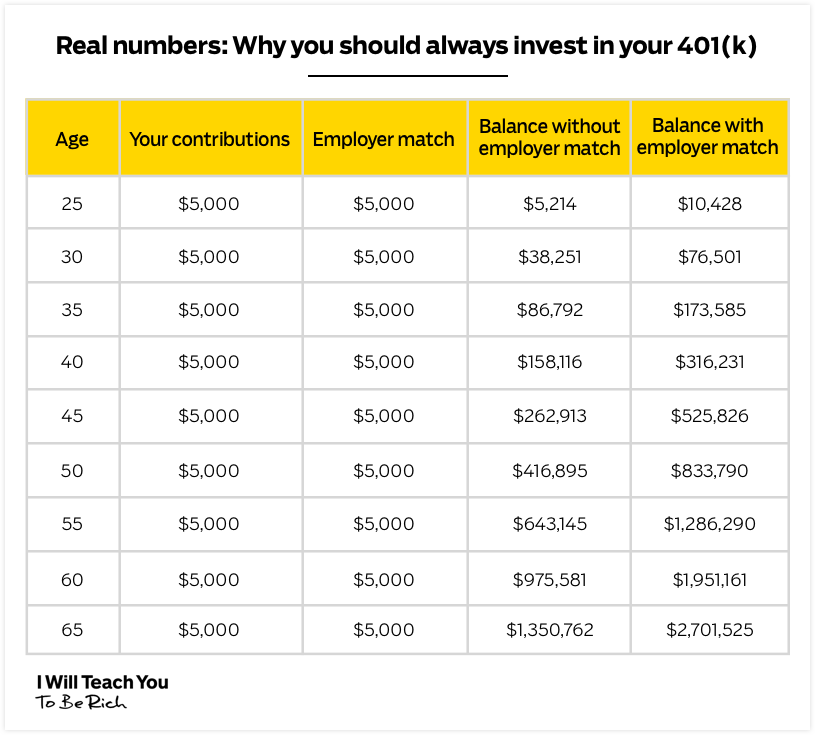

401k. Take advantage of your employer’s 401k plan by putting at least enough money to collect the employer match into it. This basically means that for every dollar you contribute, your company will match that (pre-tax!). This ensures you’re taking full advantage of what is essentially free money from your employer. That match is POWERFUL and can double your money over the course of your working life.

Debt. Once you’ve committed yourself to contributing at least the employer match for your 401k, you need to make sure you don’t have any debt. If you don’t, great! If you do, that’s okay. You can check out my system on eliminating debt fast to help you.

Roth IRA. Once you’ve started contributing to your 401k and eliminated your debt, you can start investing into a Roth IRA. Unlike your 401k, this investment account allows you to invest after-tax money and you collect no taxes on the earnings. As of writing this, you can contribute up to $5,500/year.

Once you’ve contributed up to that $5,500 limit on your Roth IRA, go back to your 401k and start contributing beyond the match. You can contribute up to $18,000/year on your 401k if you’re under 50. So you should have no issue continuing to invest in your 401k.

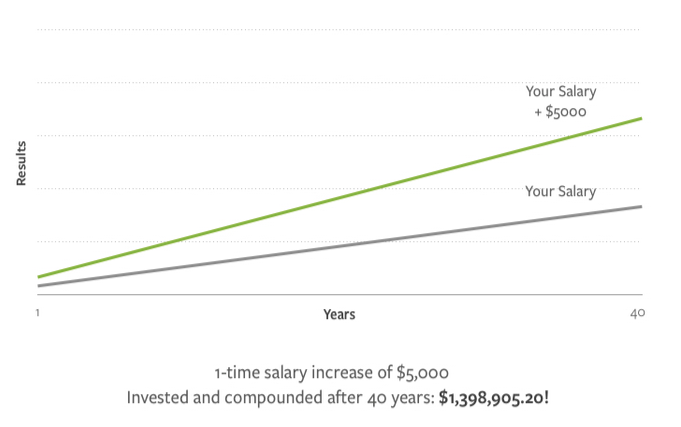

Check out how much money you stand to earn by just investing enough to get the employer’s match:

Note: If $500/month sounds like a lot, read all the ways you can free up that money with just a few phone calls.

For financial security, it’s more important than anything else to start early. And don’t worry if you think you’re a little late to the game.

My team has worked hard on something I think will help ease you into the world of investing: The Ultimate Guide to Personal Finance.

In it, you’ll learn how to:

Master your 401k. Take advantage of free money offered to you by your company … and get rich while doing it.

Manage Roth IRAs. Start saving for retirement in a worthwhile long-term investment account.

Automate your expenses. Take advantage of the wonderful magic of automation and make investing pain-free.

Enter your info below and get on your way to living a Rich Life today.

Children are expensive. But what may surprise you is children are far and away more expensive for women than men. How much does it cost to be a mother? The cost to raise a child from birth to age 18 is pegged at $250,000, but this number represents only out of pocket costs — food, clothing, extra-curricular activities, and so on. It doesn’t reflect the hidden costs and sacrifices parents make in lost income by switching to less demanding jobs, declining promotions, switching to part-time work, or even withdrawing from the workforce, temporarily or permanently. But these costs are not borne by each parent equally. Mothers disproportionately shoulder the financial, as well as physical and emotional, burden of raising children becaues they are almost always the primary caregiver. The Motherhood Tax The “Motherhood Tax” or the “Motherhood Penalty” is used to describe the financial penalty women experience for having children. […]

Knowing how much you need to retire can be the first step to saving for the future.

This begs the question: How much do I need to retire?

If you’re the average American? $1,432,775.

This means:

You could automatically have $57,311 / year and never touch your principal (in other words, you could live off the interest and never touch the $1,432,775).

This is calculated with something called The 4% Rule, which means you can safely withdraw 4% / year without running out of money.

This rule accounts for average longevity, inflation, and returns.

In short — $1.4 million will generate $57,311 / year in retirement for as long as The 4% Rule stays true.

So what if you don’t have that much? Or what if you want more?

Finances are like fingerprints: Everyone’s is unique. How much you need to retire is going to differ person to person.

Let’s take a look at how we got to that number then, and how YOU can calculate your own retirement savings goals.

To understand how much you need, you’ll need to know about The 4% Rule: This means you should be able to withdraw 4% of your savings each year when you retire without touching the principal.

This rule is based on a study from Trinity University that determined 4% is a good rate to withdraw per year for 30-year retirements.

To find out how much YOU need to retire with The 4% Rule, you simply need to:

Find out how much you spend yearly. This includes everything that you might possibly spend in a year including rent, utilities, groceries, gas, etc.

Multiply it by 25. Or however many years you anticipate being retired.

ANNUAL EXPENSES

HOW MUCH YOU NEED TO SAVE

$20,000

$500,000

$30,000

$750,000

$40,000

$1,000,000

$50,000

$1,250,000

$60,000

$1,500,000

$70,000

$1,750,000

$80,000

$2,000,000

Knowing that the average expenses for Americans total $57,311 (per HowMuch.net, using data from the Bureau of Labor Statistics), we can find the safe withdrawal rate by multiplying that by 25.

57,311 x 25 =1,432,775

So the average American requires roughly $1,432,775 in order to retire comfortably.

Remember: This is just a rule of thumb. In fact, many are quick to point out the flaws of The 4% Rule. That said, it can give you a good idea of roughly how much you need to save.

Do I have enough saved for retirement?

Like a good yoga instructor, all these numbers are flexible. This means your plans will probably change as the years pass by. You could get sick and have to take time off of work. You could win the lottery. (Won’t happen … but I got your back if you do.)

(If that last one happens, let’s hang out and drinks are on you.)

What matters is that you roll with the changes and adjust your plan accordingly — even if that means your retirement plans are pushed back a bit. Knowing your monthly savings rate removes the guesswork when life throws you a curveball.

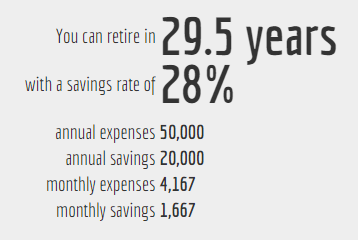

Luckily, you don’t have to strain too hard with back-of-the-napkin math to figure it out, as there are trillions of retirement calculators online. This one is great. It outlines exactly how many years it’ll take to save depending on your savings rate.

How long until I can retire with an income of $70,000

Play around with the calculator until you’ve come up with a savings rate that works for you. After that, you’ll know roughly how much you should be saving every time you get a paycheck.

How to start saving for retirement today

There are two main retirement vehicles:

Company-matched 401k. This is a powerful retirement account offered to you by your employer. With each pay period, you put a portion of your pre-tax paycheck into the account. Your company might match your contribution up to a certain percentage.

Roth IRA. A Roth IRA uses after-tax dollars to give you an even better deal. That means you put in already taxed income into stocks, bonds, or index funds and pay no taxes when you withdraw it.

Within each account, you can invest in a variety of different funds that’ll earn money for you. Which do I suggest? I’m glad you asked…

Automatic retirement savings with lifecycle funds

Target date funds (or lifecycle funds) are great funds for people who don’t want to worry about rebalancing their portfolio every year.

They work by diversifying your investments for you based on your age. And as you get older, target date funds automatically adjust your asset allocation for you.

Let’s look at an example:

If you plan to retire in about 30 years, a good target date fund for you might be the Vanguard Target Retirement 2050 Fund (VFIFX). The 2050 represents the year in which you’ll likely retire.

Since we’re still years and years away from 2050, this fund invests more in investments like stocks that are higher risk but with the potential to earn more. As we get closer to 2050 the fund automatically adjusts to invest in things like bonds, which are lower risk.

These funds aren’t for everyone though. You might have a different level of risk or different goals with your investing. However, they are designed for people who don’t want to mess around with rebalancing their portfolio at all. For you, the ease of use that comes with lifecycle funds might outweigh the loss of returns.

One thing you should note: Most lifecycle funds need between $1,000 to $3,000 to buy into them. If you don’t have that kind of money, don’t worry. I have something for you at the end that can help you get there.

For a more in-depth explanation, check out my video all about lifecycle funds.

Where should I focus my retirement investing?

How much you should actually be investing each month depends on a system I call the Ladder of Personal Finance. It looks at three areas:

Your employer’s 401k match. Each month you should be contributing as much as you need to in order to get the most out of your company’s 401k match. That means if your company offers a 5% match, you should be contributing AT LEAST 5% of your monthly income to your 401k each month.

Whether you’re in debt. Once you’ve committed yourself to contributing at least the employer match for your 401k, you need to make sure you don’t have any debt. If you don’t, great! If you do, that’s okay. You can check out my system on eliminating debt fast to help you.

Your Roth IRA contribution. Once you’ve started contributing to your 401k and eliminated your debt, you can start investing into a Roth IRA. Unlike your 401k, this investment account allows you to invest after-tax money and you collect no taxes on the earnings. As of writing this, you can contribute up to $5,500/year.

Once you’ve contributed up to that $5,500 limit on your Roth IRA, go back to your 401k and start contributing beyond the match.

“But Ramit, why would I max out my Roth IRA before my 401k if it’s so good?”

There’s a lot of nerdy debate in the personal finance sphere about this very question, but my position is based on taxes and policy.

Assuming your career goes well, you’ll be in a higher tax bracket when you retire, meaning that you’d have to pay more taxes with a 401k. Also, tax rates will likely increase in the future.

The Ladder of Personal Finance is pretty handy when considering what to prioritize when it comes to your investments. For more, check out my less than 3–minute video where I explain it.

Automate your retirement savings today

Once you have your accounts set up, it’s time to start investing — and there’s no better way to do this than with an automated system.

Automating your finances is a system that allows you to invest passively instead of you constantly wondering if you have enough money to spend.

And it’s simple: At the beginning of the month, when you receive your paycheck, the money is immediately sent to where it needs to go through automatic systems that you have set up already.

If you want to find out more about how to automate your finances, check out our 12-minute video explaining it here:

Earn more money for retirement

Knowing how much you need to retire is just the first step to saving for your future.

If you really want to ramp up your investing you need to earn more money.

Doing so will put you in the best position to retire comfortably. That’s why we here at IWT have a gift for you: The Ultimate Guide to Making Money.

In it, we’ve included our best strategies to:

Create multiple income streams so you always have a consistent source of revenue

Start your own business and escape the 9-to-5 for good

Increase your income by thousands of dollars a year through side hustles like freelancing

Download a FREE copy of the Ultimate Guide today by entering your name and email below — and jump into freelance marketing today.

The hard part of thinking about retirement is that it’s often discussed with charts and numbers in the abstract. It helps when you can see the actual steps and actual person took to save for their retirement.

To prove it, we talked to four different readers about their retirement savings. What they told us was revealing, fascinating, AND occasionally contradictory to typical investment advice.

DAKOTA, 25 – $18,000 // “I didn’t have a model for saving money.”

Income? $56,000 / year

Family? “Married. No children.”

Retirement savings? $18,000

Rent or own? Rent. $1,800 / month

What’s your job? IT coordinator at a consulting firm.

How confident do you feel about your retirement plans? I don’t feel very confident about my retirement plans so far. The amount we have saved is lower than where I’d like it to be but I know these things take time to evolve.

When did you start saving for your retirement fund? I started when I got my first full-time job out of college. It was cool because I literally started with nothing and it’s been amazing to watch it grow, even though only around $63 gets taken out of my paycheck each week.

Have you always had a saving mentality? For a lot of my adolescence we were living off of just my mom’s wages. I’m not exactly sure how much she made, it must have been less than than $30,000 a year on a waitress’s salary. And then whatever she got from my dad for child support and food stamps.

We lived paycheck to paycheck with a “we got to put food on the table” sort of mentality. So initially, I didn’t really have a model for saving money.

Did your parents have any tactics to help you get by? Mom would always bring home the food she was given for dinner to my sister and I. At the time, I never worried about what she was eating, but I know she made a lot of sacrifices to keep food on the table for us. I also never had an “allowance” like most kids get.

I did have a very frugal mindset from watching what my parents did with their money though. Once I had that surplus for the first time in my life, I started to get into the habit of saving as much as I can for the future.

What advice would you give your younger self? It doesn’t take a lot to be mindful about how much you can save. I think a lot of people get bogged down in the numbers. “Oh man, I only made $200 this pay period. I need to use this X of it just to live!” so they use the fact that saving a small amount doesn’t feel as good. BUT it can be just as impactful later on. If I saved earlier, no matter how small the amount, I would be in an even better situation now.

Also, I’d tell him to go to a cheaper school. I went to an out of state school and put myself in way more debt than I realized. I think I ended college with a little over $30,000 of debt. I could have easily gotten an associates from a local college and then went off to a university for two years to get my bachelors and saved my parents and I tens of thousands of dollars.

TIM, 30 – $327,000 // “Spend your money before you have it.”

Income? $150,000 / year

Family? “Married with one newborn.”

Rent or own? Own a house. 15-year fixed rate mortgage $2,800 / month.

What’s your job? Associate director of strategy for an insurance company.

What advice would you give your younger self when it comes to saving for retirement? Spend your money before you have it. Every Monday morning, I sit down and go through all the expenses I have for the week. I also look back at the last week to see how my expenses compares to my budget. I set up a week-by-week budget for each month too.

That’s helped me figure out that if I set away a little bit of money specifically for fun purchases like restaurants or going out, you have more money than you think to go towards saving for retirement. Making sure I knew where I wanted it to go was very important for me.

When did you start saving for retirement? I started when I was able to get a job after school. It was very basic: I contributed 6% of my income while getting a 4% employee match.

How did it evolve over time? I just kept doing that for five years until about 2014. I went from contributing enough to hit the employer contribution to enough to max out the 401k at $18,000 a year.

I don’t have a Roth IRA or anything like that.

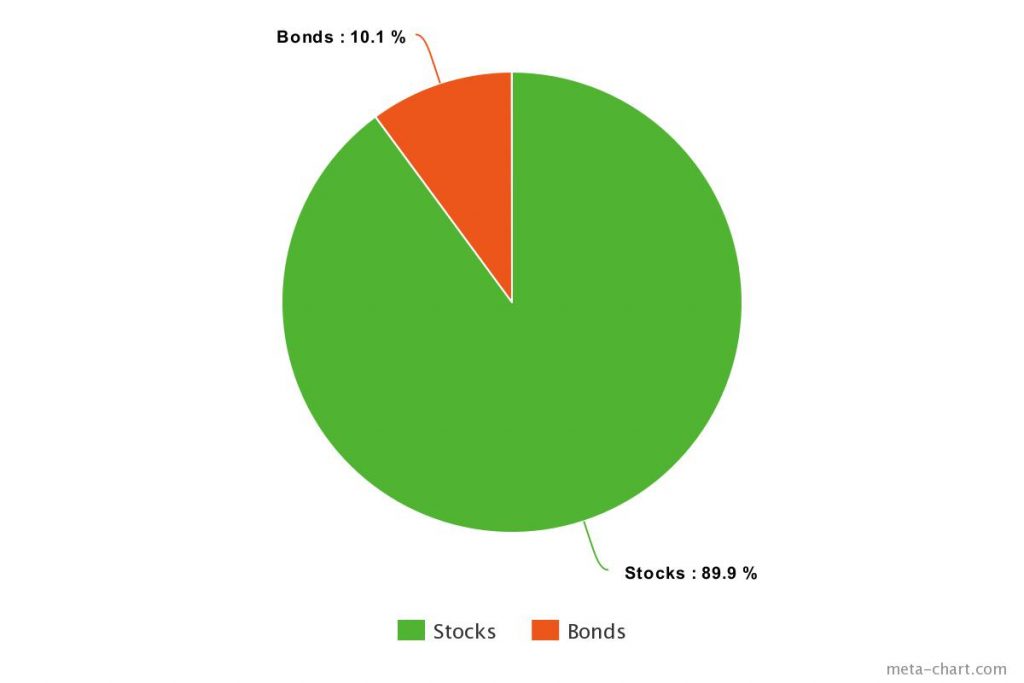

Do you feel confident about your retirement plans? Very. We’re investing very aggressively right now — we have less than 10% in bonds and the rest are in equities. We also saved about $20,000 for the baby on top of another $20,000 we have for emergencies. So if we have some unforeseen expenses come up, we have the money there.

How does your newborn impact your finances? A lot. [laughs] Our ultimate goal is to be financially independent by the time we’re 40, though to be more realistic it’ll be closer to 50. That was our plan — BUT our baby coming along threw us a curveball.

Why do you want to be financially independent? We look at the people around us — our parents, former bosses, colleagues — and they’ve spent their whole careers in this rat race doing jobs maybe they enjoyed but were ultimately grueling.

Then you get to age 60 or 65 and THEN you’re supposed to enjoy your life? We’ve seen people get there and struggle to enjoy it or not enjoy it at all. My wife and I don’t want to wait.

Is there anything keeping you from enjoying life now? I have a really good life now, so it’s not so I can enjoy my life more necessarily. It’d just give us a much greater work flexibility. It would just allow us to pursue the work that we’re really passionate about easier since we won’t have to worry about paying the bills.

What concerns you most with your retirement savings? Once we get to that point where we’re financially independent, then comes questions like, “Are my wife and I healthy enough? What if there’s an unexpected health emergency we haven’t thought about?” Then I wonder if there’s any sort of risk that we haven’t thought about that we’re not protected against.

Have you always had that fear? It goes beyond all the money we’ve saved. We’ve done all this hard work. We’ve saved all this money to protect ourselves against major financial issues … but is there something else we should be thinking about? I don’t know.

Do you feel like that’s more exasperated since having your baby? For sure. One thing we started doing differently is keeping more liquid cash on hand in case we need a safety net. Before we had our baby, I was much more concerned with putting all the extra money I had towards debt or investing it.

How much liquid cash do you have? Just under $40,000. We’re still saving for it now.

Any specific tactics that have helped you with your investing? Automating my savings. I highly suggest everyone do the same. Once you set up the money in your accounts to save automatically, you can build your life around what ends up in your personal checking account to spend. That’s huge for my wife and I. Whenever we get raises or our paychecks, we can automate it to go where it needs to go.

PETER, 32 – ~$100,000 // “Control your time now, not later.”

Income: $60,000

Family: “Married. No children.”

Rent or own: Own.

What’s your job? I work as an architect in my 9-to-5, but the thing I’m most involved in is investing through a real estate company I co-founded.

That’s very non-traditional. How has it worked out? The strategy was to buy at a reasonable price and achieve stable returns. I’d rather spend my time and money investing in areas that I have more of a control over.

What did your retirement savings look like in the beginning? I started my retirement by doing a number of things. First, I lived in my wife’s parent’s basement for four years. During that time, I worked as an architect for a firm and I saved money through a traditional 401k. I felt like I was spinning my wheels though because I felt like I didn’t have control over it. Also I had my student loans to worry about.

What are you most worried about when it comes to saving in the future? Why? I’m torn between worrying about saving too much and not saving enough. What is the right amount? How do you balance current spending with future savings?

Also things that are totally outside of my control like what happens if the real estate market crashes tomorrow? That affects the vast majority of investments I’m focused on at the moment.

Why are you worried about saving too much? You can really put yourself in a bind by saving too aggressively — especially for retirement. I think you can plan to some extent about the things that can happen but you never know what can happen. You can save and try to plan but you can really sacrifice too much of your current life if you focus on saving too aggressively.

Do you know if/when you’ll ever retire? For me, I’m viewing leaving my current job as “retiring,” because I’m going from needing to work to wanting to work. As soon as I can stop worrying about needing to work and I can focus on what I want to do, I’ll have retired.

Why don’t more view retirement this way? That’s actually something that bums me out about people’s choice when it comes to retirement. They’ll work jobs they hate for years and year and then “retire” to go do things they could have been doing the entire time.

What’s your best piece of advice for retirement savings? My wife and I have been pretty fortunate that we’ve been able to travel a lot. People always ask us, “How do you do it?” The reality is I don’t make a lot more money than they do. I just use my money intentionally.

For example, I spend money on travel and an INSANE amount of coffee, because I love those things. It actually helps you save money for things like retirement when you spend money on things you care about. It’s pretty powerful.

SCOTT, 48 – ~$500,000 // “I think we’re under.”

Income: $130,000 / year

Family: “Married with two children (ages 10 and 12).”

Rent or own: Own. 3.25% 15-year mortgage at $2,200 / month

What’s your job? I’m an interior designer and I run my own photography studio on the side.

Why are you investing so aggressively at the age of 48? We’re planning on working another 20 years until we retire. I’m not military. I don’t work for the government. I won’t have a pension.

What advice would you give to your younger self if you could? Start saving early — even if it’s just a little bit. I didn’t have as much money as I thought I should for a Roth or these other basic investments, but I should have started out with whatever it was even if it was just $50 a month. Just start. Keep it rolling. Then it’s on your radar. It is moving.

When did you start saving for your retirement fund? Right away after college. In my mid-twenties I started contributing to my employer’s 401k.

Do you feel confident with your retirement plans? No. I think we’re under. Before kids, we were really putting money away but once we had kids she got laid off from her job. Very bad luck because she was the breadwinner then.

So we had about four to five years where she was unemployed and stayed home with the kids. Our retirement could easily be double what it currently is if it weren’t for those four to five years. We missed out on an enormous amount of money.

What do you mean it could be double what it is now? It’s been 10 years since she was laid off. That income would have provided more than $1 million in gross pay. All that compounding for a decade would have made all the difference in the world.

How would you describe your life now to before your wife was laid off? While she working we made more than enough to save for our future and enjoy life – travel, eat out frequently with friends, etc.

I wouldn’t say we’ve cut out that much more, just greatly reduced the frequency. We used to spend a weekend in NYC each month, now we go maybe twice a year. We have to be a lot more thoughtful in terms of going out and socializing. Even entertaining at home can be a pricey affair. We still do these things, just less than we’d like.

How has your savings strategy changed since your wife was laid off? I’m earning more now which is good, but it’s still tough. It’s part of the reason why I started picking up my side business. It’s my “keep us sane” play money. At our age, you have to enjoy life.

What investment does your wife have? Now she runs her own marketing business, so she contributes to an SEP IRA — it’s like a Roth IRA specifically for self-employed people. The beautiful thing about that is that when you’re self employed, you’re absolutely hammered by taxes — something like 33.3% goes away! You can contribute way more to a SEP IRA than you can to a Roth IRA.

It’s a beautiful thing because it takes your taxable earnings way down.

What did you learn from becoming a one-income household? The good thing that came out of this is that we really started paying attention to our money flow. I got really obsessed with tracking our expenses and income. We got hypervigilant.

How to start saving for retirement

There’s two big takeaways from their stories I want to point out:

They all wish they started earlier. It’s so fascinating that each of the readers wished they could tell themselves to start saving earlier — no matter how little it was. If you’re reading this, and you’re still relatively young, that’s awesome! If you’re a bit older though and feel like you’re behind, don’t worry, because..

There’s no one way to do things. From Peter and Scott’s hustles to Dakota and Tim’s 401k employer match, each of these readers approach their savings differently. That means if you’re just starting that’s great. We want to show you how you can save for retirement.

Let’s talk about the two best investment tools you’ll ever have:

401k

Roth IRA

With retirement accounts, you’ll be able to accrue gains with big tax advantages with one caveat: You promise to save and invest long term. That means you can buy and sell shares of almost anything as often as you want as long as you leave the money in your account until you get near retirement age.

We’ll talk about those exceptions a little later, but for now just know that retirement accounts give you a HUGE advantage over regular investment accounts but can tie up your money in the short term, penalizing you for withdrawing before a certain date.

But what is a 401k and Roth IRA? Do you have to jump through a lot of hoops to get them? How much do you have to invest each month?

Let’s take a look at each one.

401k: Free money from your employer

A 401k is a powerful retirement account offered to you by your employer. With each pay period, you put a portion of your pre-tax paycheck into the account. That means you’re able to invest more money into a 401k than you would a regular investment account.

But here’s the best part: Your company will match you 1:1 up to a certain percentage of your paycheck.

Say your company offers 3% matching. If your yearly salary is $150,000 and you invest 3% of your yearly salary (~$5,000) into your 401k, your company would match you that amount — doubling your investment.

Check out the graph below that illustrates this.

This is free money!!! If your company offers a match, you should ABSOLUTELY take part in their 401k plan.

Where’s my money going?

When you invest in a 401k, your money goes into an investment account where a professional investing company manages it. Typically, your employer gives you different investment options to choose from (aggressive, international, mixed, etc).

Your company does most of the work when you set up the 401k and you’ll often be able to instruct them to automatically withdraw a certain amount from every paycheck. And don’t worry about switching jobs. If you should ever decide to leave your company, you can take your 401k with you.

When can I take my money out?

The money you invest in your 401k must stay in the account until you are 59 ½ years old. If you take the money out before then, you’ll get slapped with a 10% federal tax penalty on your funds.

If you want to maximize your returns for your 401k, make sure you leave it in there until you’re ready to retire. When you do take it out, you are going to have to pay income tax so it’s not completely tax-free.

But 401ks are only one part of the equation when you want to start saving for retirement. The other account you should get is a Roth IRA. And ideally, you have both.

Roth IRA: The best long-term investment

A Roth IRA is one of the best deals for long-term investing.

Remember how your 401k uses pre-tax dollars and you pay income tax when you take the money out at retirement? Well, a Roth IRA uses after-tax dollars to give you an even better deal.

With a Roth, you put in already taxed income into stocks, bonds, or index funds and pay no taxes when you withdraw it.

That’s an exceptional example, but when saving for retirement your greatest advantage is time. You have time to weather the bumps in the market. And over years, those tax-free gains are an amazing deal.

How to open a Roth IRA account

To open up a Roth IRA, find a brokerage account. There are many out there so I highly suggest shopping around and taking a look at the options out there.

Certain factors you want to consider when looking at brokers can be:

These brokers offer fantastic customer service and are well-known in the investment community for their great stock options.

Special note: Most brokers typically have minimum amounts for opening a Roth IRA, usually $3,000. Sometimes they’ll waive the minimums if you set up an automatic payment plan depositing, say, $100/month.

Also, it’s worth noting that there’s currently a yearly maximum investment of $5,500 to a Roth. (This amount changes often so be sure to check out the IRS contribution limits page to keep updated).

Once your account is set up, your money will just be sitting there. You need to do things then:

First, set up an automatic payment plan (which we’ll explain how to do later) so you’re automatically depositing money into your Roth.

Second, decide where to invest your Roth money; technically you can be in stocks, index funds, mutual funds, whatever. But we suggest investing your money in a low-cost, diversified portfolio that includes index funds such as the S&P 500. The S&P 500 averages a return of 10% and is managed with barely any fees.

Like your 401k, you’re expected to treat this as a long-term investment vehicle. You are penalized if you withdraw your earnings before you’re 59 ½ years old.

You can, however, withdraw your principal, or the amount you actually invested from your pocket, at any time, penalty-free (most people don’t know this).

There are also exceptions for down payments on a home, funding education for you/partner/children/grandchildren, and some other emergency reasons.

But it’s still a fantastic investment to make — especially when you do it early. After all, the sooner you can invest, the more money your investment will accrue.

Automate your finances for pain-free investments

Once you have your accounts set up, it’s time to start investing — and there’s no better way to do this than with an automated system.

Automating your finances is a system that allows you to invest passively instead of you constantly wondering if you have enough money to spend.

And it’s simple: At the beginning of the month, when you receive your paycheck, the money is immediately sent to where it needs to go through automatic systems that you have set up already.

If you want to find out more on how to automate your finances, check out our 12-minute video explaining it here:

Beat the average retirement savings

Once you have your system automated and you’re investing consistently into your Roth IRA and 401k, then congrats! You’re already ahead of 99% of the population when it comes to taking control of your personal finances — and on your way to beating the average retirement savings.

You’re well on your way to wealth and living a Rich Life — but it shouldn’t stop there.

Ramit goes into even more detail on investing in Chapter 7 of my New York Times best-selling book, I Will Teach You To Be Rich.

You can get the entire chapter, free, below. In it, he covers the nitty-gritty of maintaining your investment accounts, asset allocation, and rebalancing your portfolio to maximize returns.

I know: There’s a ton to cover here about making the most out of these accounts, but if you’re a weirdo IWT reader, you’ll love learning about it.

Asking for a promotion is an extremely stressful moment in your career.

“What if they say no?”

“What if they laugh me out of the room?”

“What if they don’t see the value I add to the company?”

Just thinking of the possible answers can make you sick.

But if you’ve tackled larger workloads and added tremendous value, shouldn’t your job title adequately reflect your increased value?

It’s time to ask for a promotion or a raise.

You’re going to learn exactly how to turn a typically uncomfortable conversation into an enjoyable discussion and how to make this a no-brainer decision for your boss.

Knowing how to ask for a promotion can make you rich

Consider these three points:

A promotion conversation can take as little as 10 minutes.

A promotion can propel you to the next level in your career.

Many of my students and friends who’ve used the techniques I’m going to share have learned how to ask for raises of $10,000 or more.

Even if a promotion only gets you half of that (a $5,000 raise), it adds up dramatically over time.

Take a look:

And remember — most people who get a promotion once tend to get promoted frequently!

Asking for a promotion is a smart and time-effective way to put more money in your pocket and improve your career.

So why do most people leave their career trajectory to chance? Simple: Fear. Most are afraid they’re going to be shot down so they don’t even try.

Luckily, you can combat this fear with some preparation.

How to define your value to your employer (you’re probably doing too much)

How long have you been at your company?

2 years? 5 years? 10 years? Let’s just assume it’s been awhile.

During that time, you’ve definitely gotten better at your job. You’ve probably developed new skills and you’ve taken on new responsibilities. You’re probably helping the company much more than you did a year ago. So while your contribution continues to rise, your compensation has remained stagnant.

Many of us are humble and modest by nature — and that’s okay. But there’s a BIG difference between being humble and undervaluing yourself:

Humble: “I’ve done XYZ, and I’m proud of that accomplishment.”

Undervaluing: “Oh sure, I kinda helped out with that project, but it wasn’t just me. Besides, anybody could have done that, so why should I feel special?”

And as the bard once wrote…

Here’s an exercise you can do to break this limiting belief: List all the ways that you’ve become more valuable to the company since you started your job.

Be generous with your list, but push yourself to get specific:

Have you delivered specific results? Which ones? Estimate how much they were worth.

Has your communication improved? How so?

Are you more efficient than before? How do you know?

Do you know the business better? How does this translate to the company’s bottom line?

Have you developed new skills? What kind?

Keep in mind that achievements that seem mundane to you might seem exceptional to someone else. No achievement is too small. Write them all down.

This is your first step in learning how to ask for a raise or a promotion.

Now that you know the value you add, it’s time to prepare for the conversation with your boss.

The #1 mistake when asking for a promotion (or raise)

The absolute WORST mistake you can make when it comes to how to ask for a raise or promotion is to simply show up on the day of your performance review and ask for it.

If this is your plan, you will lose.

And what’s more, you deserve to lose.

I learned this lesson the hard way. When I was a student at Stanford, I did some work for a local venture capital firm. After a few months, I decided that I was going to ask my boss for a promotion — after all, I’m a smart guy and I’ve been working pretty hard, so I should ask, right?

The conversation went something like this:

Ramit: “Hi Boss, thanks for meeting with me. So, I’ve been working here for a few months now, and I think I’ve been doing a really good job. I’ve really gotten a good understanding of the ins and outs of the business, and because of that I’d like to discuss with you the possibility of a promotion.”

Boss: “Why do you think I should give you a promotion?”

Ramit: “Well … you know, as I mentioned, I think I’ve been doing a really good job, and I’ve been learning a lot about the company and how everything works here and … yeah.”

Boss: “No. Not gonna happen.”

Ramit: “Oh. Okay.”

It wasn’t pretty. And I was actually mad at my boss about it for two whole days (he said “NO!!’).

But then I realized I was being ridiculous. I hadn’t given him any legitimate reasons why he should be giving me more responsibility and paying me more. So why would I have expected him to?

I’ve gotten a lot better at negotiation since then, and this is the #1 rule I’ve discovered about negotiation:

80% of the work in a negotiation is done before you ever walk into the room

That means the conversation is only a small fraction of what actually makes or breaks the negotiation. In reality, when you’re learning how to ask for a raise or a promotion, it’s your PREPARATION that will determine whether you succeed or fail.

Put it another way, would you rather spend zero hours preparing and get immediately blown out of a negotiation — or would you be willing to spend 20 hours of preparation with a 70% chance of successfully negotiating a raise or a promotion?

Front-loading the work

Top performers are willing to put in the time and effort, which is why they can reap disproportionate rewards.

Doing amazing work for at least three to six months, with written praise collected from your coworkers and your own boss.

Creating a five-page document of proof of performance, showing all the ways you’ve added value above and beyond your job’s requirements.

Practicing with another skilled negotiator, recording that on video, preparing for every contingency and objection that your boss might have.

Once you’ve put in the work and have done a decent amount of preparation, you’ll want to make sure your boss knows you plan on asking for a raise or promotion.

The timeline for negotiation

How long would it take for you to go from an average performer (where you are now) to a Top Performer (ready to negotiate your first raise)?

Three to six months in most cases. Sometimes more, sometimes less, but three to six months is usually an achievable goal.

This tends to surprise people.

“How can I negotiate my salary three months from now? I’m just lucky to have a job.”

If you’re a Top Performer, the time that you’re at the company won’t matter as much as the work you’re putting in.

This mindset is crucial to knowing your worth. If you’re skeptical of your own value, your boss will instantly ferret it out, costing you thousands of dollars.

It is possible to demonstrate massive tremendous value in three months — even as a new graduate. Even with few skills. Even in a crappy economy.

I’ll show you how to pick ambitious goals that actually matter to your boss and work collaboratively to achieve them. These goals will be strategic to negotiating a raise, all within a tight timeline.

And here’s what those three to six months would look like:

If you don’t get a regularly scheduled performance review, don’t worry — I’ll provide all the scripts you need to get your boss to agree to a salary conversation. But the basic idea behind your Negotiation Timeline is this:

3-6 months before your review: Become a Top Performer by collaboratively setting expectations with your boss, then exceeding those expectations in every way possible.

1-2 months before your review: Prepare the Briefcase Technique of evidence to support the exact reasons why you should be given a raise.

1-2 weeks before your review: Practice extensively with the right tactics and scripts.

Notice that all of this is done BEFORE the actual meeting (of course, your friends will only see the results you got, not all the work you put in).

This timeline positions you best to ask for a raise or promotion.

Let’s start by learning how to set expectations for your boss.

3 – 6 months out: Prepare your boss for giving you a promotion by setting expectations

Your boss should NEVER be surprised by you asking for a promotion or a raise. If they are, you did something wrong and your chances for success drop dramatically.

Think about it: If you simply blindside your boss, you’re putting him or her on the spot.

Nobody likes being cornered, especially regarding money and promotions. Their natural reaction will be to become defensive. In psychological parlance, they’ll experience “reactance” (which is a fancy way of saying “no way, Jose”).

Instead, prepare your boss for giving you a promotion. I walk through exactly how to do this in this video:

Once your boss is prepared it’s time to prepare the Briefcase Technique.

1 – 2 months out: Prepare the Briefcase Technique to nail your negotiations

This is one of my absolute favorite techniques to utilize in interviews, salary negotiations, client proposals — whatever!

First, you’re going to create a one to five page proposal document showcasing the specific areas in the company wherein you can add value.

Then, you’re going to bring the proposal with you when you negotiate your salary. When the question of compensation inevitably arises, you’re going to pull out this document and outline exactly how you’re going to solve the challenges of the company.

Hiring manager: So what’s your price range?

You: Actually, before we discuss compensation, I’d love to show you something I put together.

And then you literally pull out your proposal document detailing the pain points of the company and EXACTLY how you can help them. (Bonus points if you actually use a briefcase.)

By identifying the pain points the company is experiencing, you can show the hiring manager where specifically you’re going to add value — making you a very valuable hire.

Approach the proposal as the most compelling menu they’ve ever received — complete with issues that they know about and how YOU are the person to solve those problems.

I go into even more detail on the Briefcase Technique in this two-minute video. Check it out below.

1 – 2 weeks out: Practice, practice, practice

The last step before your negotiation is to practice, practice, and practice some more.

It’s one thing to read about how to negotiate. Actually doing it, live and under pressure, is another experience altogether. The only solution is practice.

Amazingly, most people never do this. They simply consume information and think, “Yeah yeah, I got it,” or “I’ll do it later.” But they never follow through. Yet as little as one to two hours of practice could mean the difference between success and failure.

Here’s how to do it: First, sit in front of a video camera, either alone or with a friend. Then brainstorm as many different potential scenarios as possible and practice your responses live and out loud, just as you would in front of your boss.

For example, you might practice what you’d say if:

Your boss acts surprised or annoyed when you bring up salary.

Your boss asks you to name a number first.

He tries to turn you down with excuses like “It’s the economy” or “Everyone else is getting the same thing.”

Then, observe (or have a friend give feedback on) the following, and practice until perfect:

Your words. They should be compelling and concise, and free of rambling sentences.

Your body language. You want to be sitting up, leaning forward, and relaxed.

Your tone. It should be professional, positive, and energetic.

This works. I know because I used to suck in interviews and negotiations. I had no idea how to ask for a raise or promotion — but then I started practicing.

When I was in high school, I was having trouble landing any scholarships, even though I thought I was acing the in-person interviews.

It wasn’t until I recorded myself practicing on video that I realized the problem: I never smiled. I seemed stern and unfriendly. When I started smiling regularly, I started to nail scholarship after scholarship — enough to pay my way through undergrad and grad school at Stanford.

A while back, I decided I wanted to get better at doing TV interviews, so I got some help from professional media trainers. Again, I thought I was already pretty good. But in my very first videotaped answer, the trainers showed me about a dozen subtle mistakes I was making.

They showed me how to correct them and we tried again and again. After each round, they showed me the before-and-after video. The difference was night and day.

See for yourself the difference that even a few minutes of practice can make:

How to ask for a raise and boost your salary

The Boys Scouts know it. The Lion King knows it. And now, YOU know it.

Be prepared.

It’s the most important element when it comes to how to ask for a raise or promotion. With a little bit of preparation, you’ll be ahead of 99.9% of the population — instantly improving your chances of nailing your negotiations.

If you’ve made it to this stage, the final step is knowing simply what to say when you finally ask your boss for a promotion. You want to make the conversation flow as smoothly as possible. The discussion should be mutually beneficial so your boss sees the tremendous value you’ve delivered.

I’ve gone the extra step and included word-for-word negotiation scripts here. Now, you’ll walk into your discussion confident and skyrocket your odds of getting a better title and a better salary.