What is a bad credit score (and what to do about it)

The world of credit scores can be confusing. It’s filled with esoteric jargon like “credit risk” and “FICO.”

I want to help you cut through all the BS and get down to one really important question:

What is a bad credit score?

The answer? Anything less than 670.

Anything below 670 and you’re at risk for higher interest rates on loans (if you get approved at all), getting denied an apartment rental, or even passed up on a job application.

But there is hope. You can improve your credit score even if your score is less than 670.

We know because we talked to someone who has been there.

How this entrepreneur crawled out of debt and escaped her bad credit score

Credit score then: 600 – 650

Credit score now: 789

Debt owed: $12,000 in credit card debt and $35,000 in student loans

Meet Kelsey Jones.

Kelsey is a writer, entrepreneur, and founder of a marketing company called Six Stories. Though her business is thriving and she and her husband are on solid financial footing, that wasn’t always the case.

In fact, her credit score took an absolute beating after college due to a problem that happens to many college students: They don’t understand how credit cards work.

This put her in a prime position to fall into debt and kill her credit score before she even graduated.

“I got one of those credit cards you get at a tent with a free t-shirt,” she says. “My parents told me nothing about credit card debt and managing money as I’m sure most don’t, so I had no idea how to manage a credit card and use it to my advantage.”

Due to her inexperience with cards, she didn’t understand the dangers. Like many people with bad credit, she was drawn in by flashy sign-up offers and bonuses. She wound up opening credit cards at stores such as American Eagle and Victoria’s Secret, as well as the major card companies like American Express and Discover.

This behavior eventually led to a sizeable amount of credit card debt. Kelly wound up owing roughly $12,000 in credit card debt when she graduated in 2008 on top of the $35,000 she owed for student loans.

Her credit score soon plummeted — and was further exacerbated by late payments.

“I sometimes paid my bills late because I just didn’t have enough money,” she says. “I was so broke when I graduated! I vividly remember my paychecks every two weeks were only $730. Meanwhile, I had to pay for my one-bedroom studio, car, cell phone, and all the other bills that come from truly being on your own.”

She adds, “My rent was almost the equivalent of one entire paycheck!”

I felt like I was “less than”

Being in debt and having your credit card debt can take a mental and emotional toll on you as well as a financial one. In fact, researchers have found that there’s a strong correlation between debt and mental health issues.

Debt can be both the cause and symptom of depression and anxiety — and it’s only exacerbated by the fact that many just want to ignore their financial problems.

“I buried my head in the sand for a long time,” she says. “I justified it for a while so I didn’t have to confront the angry feelings I had at myself for getting myself in that situation — specifically from credit card debt.”

For anyone who has ever been in debt, this feeling of anger and guilt should be familiar. When combined, it creates a potent mix that can be debilitating leading to inaction.

That’s why the first step in our system to getting out of debt fast is simply finding out how much you owe. When you confront your debt head-on, you provide yourself with a powerful mental boost that can help you eliminate it completely.

For Kelsey, though, that was easier said than done.

“I felt like I was ‘less than’ because I couldn’t get my shit together well enough to really take care of it,” Kelsey explains. “I felt so out of control of my life and wasn’t ready to be so broke after college. For some reason, I thought things would automatically get better, without me actually having to do anything.”

The wake-up call

It wasn’t until one day when her husband sat her down that she finally had a frank discussion about her finances: Something needed to change.

“Him coming to me about my debt was a wake-up call for me,” she says. “I couldn’t hide anymore.”

Debt is one of the biggest and most common barriers to living a Rich Life. And in their discussion, Kelsey realized that it was getting in the way of everything she and her husband wanted in their lives.

“I wanted to stop being a victim,” she says, “and dreading everything to do with money.”

Credit score improvement game plan

Kelsey’s plan to improve her credit score and escape her financial advice was threefold.

Step 1: Set a goal

First, Kelsey made the conscious decision to escape debt.

“I decided that this was it,” she says. “I was done being in debt. You have to make the conscious decision that you are done being ‘that person.’”

Though it may seem like a no-brainer, many people still put their heads in the sand and avoid their situation entirely — but that’s exactly what your lenders want you to do. They want you to avoid your statements. They want you to just pay off the minimum every month so you owe more interest. That’s how they make money.

Which is why one of our first steps in our credit score improvement system is to find out how much you owe. Once you do that, you’ll know how you can approach paying off your debts.

For Kelsey, the decision to confront her debt was a game changer.

“I went to Staples and bought a huge piece of poster board and bright markers and hung it up in my office,” she says. “I created a bar chart with months at the bottom and debt amount on the side. At the end of every month, I updated the poster board with different colors. It was awesome to see the bar graph trend down.”

Kelsey began to obsess over crushing her debt. She even leveraged this debt calculator spreadsheet whenever she made a financial transaction.

“I constantly updated it when I made payments and even made extra copies of it to test scenarios like ‘What would happen if I paid extra on my Discover card payment?’ or ‘What if I paid off this loan versus the other one?’” she explains. “Just knowing I could be debt-free in X number of months kept me going.”

Step 2: Pay down the debt by any means necessary

Kelsey also made sure that every piece of extra money she received went towards paying down her debt. This meant sacrificing a few things she loved in order to do it.

“We didn’t go on any trips and I didn’t go out to eat with friends as often as I used to,” she explains. “I still didn’t deprive myself, I simply cut down a little.”

She continues, “Any additional extra money, like tax returns, birthday gifts, and even the brand new MacBook I won in a contest, all went toward debt. It was extremely sad to ship that new MacBook to its new owner after I sold it on eBay — but I was obsessed.”

Step 3: Earn more money

Kelsey also leveraged a tried-and-true IWT method of attaining a Rich Life: Earning more money.

“I had my own digital marketing business at this time,” she recalls. “So the amount of money I made was completely up to me. I went into overdrive mode. I asked existing clients for more work and I sent pitch after pitch to potential new clients. I worked probably 50 hours a week … often until 9 or 10 at night and on the weekends, to hit my goals.”

The results

This diligence and hustle ultimately paid off when nearly two years later, she found herself debt-free.

“I still vividly remember sitting on my bed and submitting that last payment to Sallie Mae,” she says. “I promptly had a dance party in my bedroom for a few minutes, and then immediately started making my credit cards work for me.”

That meant putting in place a proven system of (say it with me):

“I set all recurring bills I could to be paid via credit card for the points and I paid off the balances completely each month,” Kelsey says. “Knowing how hard I worked to pay off that debt, I never wanted to get into that situation again. Now, about five years later, I still have never carried a balance over on a credit card more than one time.”

And to people with a low credit score, Kelsey has three pieces of advice:

Stop lying to yourself or justifying it.By confronting the uncomfortable truths about your credit score, you can take the steps to improve it. “Put yourself on an all cash budget or open a new checking account that only has your spending money for groceries, fun, etc.,” she suggests. “Your other checking account can be used to pay your credit card balances and other bills like rent.”

Ask yourself, “Where do I want to be a year from now?” It’s easy to make bad financial decisions when you don’t keep the end goal in mind. “Think about if going into more debt is worth it,” Kelsey says. “Will that new computer really make you feel better or will you feel worse because you’re even more behind on your debt?”

Think about your loved ones. Often times, debt doesn’t only affect you. It also affects your loved ones. “Having a child with our income and debt I had would’ve been irresponsible […] Think about how your debt could impact your spouse and your freedom as a family to make decisions and move forward in life.”

Now that Kelsey’s out of debt and she has a good credit score, she’s now in a great position to live her Rich Life.

What is a bad credit score?

Just like with Kelsey, a bad credit score can be emblematic of many financial issues. To understand why a credit score like 670 is bad though, you need to understand how credit scores work.

Your credit score is a number that lenders use to determine how much of a risk it is to lend to you.

This number will typically be between 300 and 850. The higher your credit score, the better you are situated for things like home and car loans.

The actual number is determined by the following information and their associated weight in relation to your score (credit score formula courtesy of Wells Fargo):

Payment history: 35%

Amounts owed: 30%

Length of credit history: 15%

How many types of credit in use: 10%

Account inquiries: 10%

Check out these ranges from Experian, one of the three main credit reporting bureaus, to see how your credit score shapes up:

800 – 850 (Great credit score). I want to take this credit score out to a nice seafood dinner, propose marriage to it, and live out our days in the country. It’s that good. If your credit score is in this range, you’ll have no problems getting a home loan or nailing a fantastic interest rate on your mortgage.

740 – 799 (Good credit score). The credit score you’d be happy to bring home to your parents. This is a pretty good spot to be. Though it’s not the best, you’ll still have no problem getting approved for loans and attaining good interest rates.

670 – 739 (Okay credit score). This credit score range is fine for the short term, but you’re going to want to upgrade soon. At this point, any hit to your credit score will be a bad one.

580 – 669 (Bad credit score). In this range, you’re considered a “subprime borrower,” which means you’re likely not to be considered for a loan at all and will struggle getting approved for simple things like apartments.

300 – 579 (Really bad credit score). Immediate swipe left on this credit score. In fact, delete the app entirely. You are a “deep subprime borrower” and won’t get any good rates and won’t likely get approved for any loans. You’ll want to stick around to find out how exactly you can improve your score.

If you want to be approved for any conventional mortgage, you’re going to need a credit score of at least 620. That’s why any credit score below 670 is a bad credit score. At that point, even the smallest hit to your credit score can affect your interest rates and loan approvals.

Miss a payment? Those missing payments affect 35% of your score.

Close down a credit card? That affects 10% of your score.

Even the lender simply opening up an inquiry to your credit hits your score by 10%.

That’s why it’s so important to be aware of your credit score and improve it when it’s bad.

“I have a bad credit score! What should I do?”

If your credit score is bad, you’re not alone. Nearly a third of Americans have a credit score of less than 600.

Also, there’s a chance that you might even be typical for your age range. Check out the average credit score by age as of early 2017 (courtesy of Time):

Age range

Credit score

18 – 29

652

30 – 39

671

40 – 49

685

50 – 59

709

60+

743

No matter what your credit score is, remember one thing: No credit score is too low to improve.

We want to help you do just that by taking a look at someone who had a low credit score — and the exact steps they took to improve it.

What is a bad credit score? The one that stops you from your Rich Life.

Debt is the number one barrier to living your Rich Life. If you’re in debt and have a bad credit score, we want to help you.

Check out our resources below to get started improving your credit score today:

Be sure to check out Ramit’s video on negotiating your debt too so you can pay it off even faster.

To help you even more, we’d like to offer you something: The first chapter of Ramit’s New York Timesbest-seller “I Will Teach You to Be Rich.”

It’ll help you tap into even more perks, max out your rewards, and beat the credit card companies at their own game.

It includes the tools and word-for-word scripts to fight back against the huge credit card companies. To download it free now, enter your name and email below.

Good side hustle ideas can open the door to unlimited earning potential.

However, we have limited willpower as humans.

Think about how so many of us go about doing something like creating a side hustle:

Stage 1: Decide you want to have a side hustle. (“I think I want to have a side business so I’m my own boss!”)

Stage 2: Get excited about the prospect of earning more money. (“I can’t wait to do what I love AND get more money! I wonder how much tickets to Cabo are this time of year?”)

Stage 3: Try to come up with side hustle ideas. (“But wait, what’s my business going to be?”)

Stage 4: Get overwhelmed, dejected, and give up. (“I can’t come up with a good idea. I guess I’ll just keep working for my boss…”)

We’re not going to do that though. Instead, I’m going to show you exactly how you can create your own side hustle AND give you a list of great side hustle ideas as a launching point.

One thing I’m sick of are listicles online that tout the “3,000 best side hustle ideas” but most of them are trash.

You know the ones I’m talking about too.

“Have a garage sale!”

“Sell your hair for cash!”

“Take online surveys that’ll pay you literally DOZENS of cents!”

These “hustles” are vague, non-scalable, and just not worth your time. Instead, I’d like you to reframe what you’re looking for. You’re not looking for an idea. You are focused on finding your inner expertise.

What do I mean? We all have skills and talents that are 100% marketable, but most of us don’t even realize it.

I went to this party while I was in college once and there was this guy there drinking heavily. I’m talking seven shots in with more to come. Later, I’m looking at his bookshelf (because I’m a weirdo) and find a neuroanatomy textbook.

This guy was in the process of killing hundreds of his own brain cells — but he’s also smart enough to save another person’s brain cells. You wouldn’t know he was this very talented and smart dude by just looking at him though.

That’s because those skills were his inner expertise — and you have them too.

All you have to do is ask yourself some very simple questions:

Question #1: What knowledge have I acquired?

We pay to learn a lot of things:

College degrees

Spanish language lessons

Yoga classes

Guitar lessons

Improv classes

Writing workshops

We pay for all of this because we know it’s more efficient to learn things by paying money for expert knowledge.

Guess what? You can be that teacher too.

And I know what you’re thinking: “I’m not good enough at anything to teach anyone else.” Look, there are plenty of people who aren’t “as good” as other people in certain skills but they’re still making money off of their knowledge.

Do you think James Patterson is the BEST writer?

Do you think Dwayne “The Rock” Johnson is the BEST actor?

How about that popular Mexican restaurant a few blocks from you. Do you think they have the BEST burritos?

No — but these people are still making money off their knowledge. And there are things that you can turn into marketable side hustle ideas too.

What knowledge do you have to turn into a side hustle?

Question #2: What do I do on a Saturday morning?

The answer to this question reveals what you’re passionate about and what people might pay you for. Because we all have something we just love doing on Saturday mornings before everyone else is awake.

I have a friend who LOVES clothes. Her Saturday mornings consist of reading fashion blogs and maintaining a Pinterest account overflowing with outfit and design ideas.

Here’s what I find interesting: She never thought about turning this into a business! It’s just something she likes to do BUT I guarantee you that there are a lot of people who’d pay $500 for a style consultation over Skype that she could do from the comfort of her own home. Some people might even pay her thousands to be their personal shopper.

Something that my friend loves doing for fun on a Saturday morning could be turned into a thriving business with a few key systems (more on that later). So ask yourself: What do I like to do in my free time?

Are you at the gym or training for marathons as a hobby? People would pay you for your fitness knowledge.

Do you love reading dating advice blogs or browsing /r/relationships? You could give relationship advice or coaching to the lovelorn.

Maybe you like working on your car in your free time. People would pay you to fix their car troubles too!

What you do when you have a ton of downtime is a great indicator of your passions and talents.

Question #3: What challenges have I overcome?

We can turn our most painful and vulnerable moments into a great side hustle.

Don’t believe me? Check out all of these profitable hustles that came out of challenges people have faced:

CrohnsColitisLifestyle.com.After Dane Johnson was diagnosed with Crohn’s/Colitis, he devoted himself to helping people with the disease achieve their fitness and nutrition goals.

JenTurrell.com.When her eldest daughter was born, Jen discovered her daughter had autism. Her life soon became a whirlwind of tough financial decisions and sacrifices. She now uses the knowledge she gained during her experience to help other women find their financial footing as well.

FindYourInnerHappy.com.Tree Franklyn always struggled with handling her emotions — until she learned a great system to deal with her sensitive nature. Now she helps women manage their emotions so they don’t feel overwhelmed all the time.

While it may be tough to revisit some of those painful moments, it’s also empowering knowing that you overcame it AND can help others in their struggles too.

So what have YOU struggled with that you can help others with too?

Did you struggle to lose weight for years and figured out how to get in shape?

Are you an introvert who has learned to overcome shyness to become more sociable?

Have you failed test after test before learning an amazing study technique?

Find an answer to this question and I promise you you’ll find a profitable business idea.

Action step: Come up with 20 ideas

It’s time to figure out what exactly you’re good at and put it down on paper. We start by doing an inventory of everything — our knowledge, passions, and challenges we’ve overcome.

So answer each question below and come up with a few ideas for each until you have 20 answers in all.

What knowledge have I acquired?

What do I do on a Saturday morning?

What challenges have I overcome?

It’s okay if it’s not an even number of answers (unless you can come up with 6.666667 answers for each one). What’s important is that you’ve put down 20 on paper.

Put aside 30 minutes today and 30 minutes tomorrow to do this. Literally block them out on your calendar and protect that time. You can do this RIGHT now.

Make sure there are TWO distinct times you do this. That’s because when you step away from a problem, you free up a different part of your mind that helps you problem solve more effectively.

Once you’re done, congrats! You’re well on your way to getting started earning money with your side hustle ideas.

How to keep motivated with your side hustle ideas

Many people can get overwhelmed after coming up with their 20 side hustle ideas — and I don’t blame them. Taking your side hustle ideas and running with them takes a lot of time and determination.

BUT I promise you that it’s completely worth it. Three reasons why:

Most people don’t even think to earn more — giving you an edge. Because of differences in skill, motivation, and luck, few people ever try to earn more. Instead, they choose to complain about things they can’t control like the economy and taxes while focusing on things like cutting out lattes to save money.

So if you’re in that small group of motivated hustlers who do actually earn more, you earn the lion’s share of side revenue. When you pick an area to excel where there’s a built-in barrier to success — like earning more money on the side — the winners get disproportionate winnings.

Mitigate your risks. What if you lost your job tomorrow? Would you have another source of income to fall back on? If not, you’re going to have to dip into your emergency fund … if you have one that is.

Just like with your portfolio, you know about the importance of diversifying your investments. It’s the same idea when it comes to your revenue sources.

Managing your money and earning more money is a powerful combination. Combine earning more with the automation strategy for saving, investing, and spending that I outline in my book, and you’ll have a powerful financial combination guaranteed to set you up for a Rich Life.

If you’re still nervous about your side hustle ideas, I want to help you even more with a bonus:

BONUS: 42 side hustle ideas for beginners, college students, parents, and more!

No matter your employment, family status, or location, you can find the right business idea to pursue on the side. To help you get started even more, here are 42 examples of great hustles you can start today.

Side hustle ideas for beginners

Here is a list of services that don’t take any special skills or training at all that you can offer to people for money:

Transcription services

Courier services

Cooking / personal chef

Technical writing

Small business marketing

Proofreading / editing

Business writing (business plans, grants white papers)

Side hustle ideas for college students

You can start a lucrative side hustle even if you’re living in a dorm room right now. Actually, that’s how I started IWT over a decade ago. Check out these hustles:

Video production / editing

Design (brochures, business cards, logos, newsletters)

Web design

Blogging / blog consulting

Sports / personal training

Child care

Search engine optimization (SEO)

Side hustle ideas for millennials

Millennials have a wealth of marketable skills just by virtue of being in a tech-centric generation. My first side hustle was consulting for venture capital firms on how young people were using social media. Here are some other things you can do:

User interface & user experience (UI/UX)

Google Analytics

Programming / web development

E-commerce consulting

Tech tutoring (e.g., how to set up and use your tablet)

Internet marketing consulting

Fashion / image consulting

Side hustle ideas for stay-at-home parents

Parents have some of the busiest schedules and irregular hours of anyone. However, on top of all those responsibilities, you can find a side hustle idea that makes your money. Case in point:

Personal / virtual assistant

Pet services (grooming, walking, etc.)

Home maintenance

Crafting / personalization services

Human resources / payroll services

Project management / productivity consulting

Copywriting and editing

Side hustle ideas for working parents

If you’re a working parent, you probably have skills such as planning, budgeting, and productivity. You can easily transform one of those skills into a side hustle such as:

Photography

Travel planning

Event planning / promotion

Automobile / motorcycle repair

Tax and financial planning

Community management / promotion

Career help (finding work, optimizing resumes, cover letters, etc.)

Side hustle ideas for teachers

Teaching and the skills involved are at the core of a lot of thriving side hustles. That’s why professional teachers have an advantage when it comes to hustles such as:

Research

Presentation design (e.g., PowerPoint)

Tutoring and coaching

SAT prep

College application review

Productivity coaching

Accounting / bookkeeping

“I have my side hustle ideas … what now?”

Once you have your side hustle ideas, it’s time to start putting your ideas to work for you — and you do that by finding your first client/customer/person-who-will-throw-money-at-you-for-your-service.

Without your customer, your side hustle ideas will remain just that — ideas. And while it may seem daunting to start selling your skills, it’s actually pretty straightforward as long as you have the right systems.

That’s why I want to offer you my guide to get you started:

Find Your First Client in the Next 6 Weeks

I’ve included some of my best techniques and strategies on finding a client who will pay you money for your skills in less than two months.

Enter your information below and I’ll send you the FREE guide right to your inbox.

Be sure to tweet your results at me @ramit. Check out this one I got from a reader recently:

I can’t wait to hear about your awesome side hustle ideas.

As you may have already heard, I recently ruined my credit score. I was using Borrowell to monitor it for free, and after 3 months of it going down, I finally checked to see what was going on. Luckily, the loss of more than 150 points to my credit score was due to a small error that was fixed even faster than it happened. But for those months that I watched it nosedive off a cliff, I experienced some SERIOUS financial stress. Want to know where you stand? Request your free credit score & credit report from Borrowell HERE! Now that my score is fixed, I can rest easy… and never go a single month without checking it ever again. Why is your credit score important? Your credit score is more or less a risk assessment of how good you are at managing debt. Lenders use it to determine if […]

Real estate investing can be a great way to make a lot of money if you do your research and are prepared to devote a lot of time to your investments.

However, it’s also a great way for investors to lose money. I believe that real estate is one of the most overrated investments in America, and very few will show you real numbers to explain why.

That’s why I want to break down the facets of real estate investing, show you a few ways you can get started (if you want to), and reveal the myths behind real estate that you won’t hear anywhere else.

Here are three ways you can approach real estate investing:

Investing in a REIT

Buying a rental property

Flipping properties

Some ways are better than others depending on your financial situation and goals. While I’m not a fan of real estate investing, I do believe that if you’re going to do it, you should understand your options.

Real estate investing #1: A REIT

REITs, or real estate investment trusts, are a good choice if you want to get involved with real estate investing but don’t want to make the huge commitment of purchasing a property.

That’s because REITs are like the mutual funds of real estate. They’re a collection of properties operated by a company (aka a trust) that leverages money from individual investors to buy and develop real estate. And investors get paid in dividends with REITs just like any other fund. And you, too, can be one of those individual investors.

REITs can focus on a variety of different industries both domestically and internationally, and you can invest in REITs that invest in apartments, business buildings, or even healthcare facilities.

In all, they are an easy and straightforward way to get involved with real estate investing without having to put up an enormous upfront cost of actually buying property. To get started, you just have to go to your online broker and purchase a REIT like you would your typical investments.

If you don’t know how to do that, that’s okay! Check out our article on mutual funds to find out exactly how you can open one.

But let’s say that you have $30,000+ just burning a hole in your pocket. If you’re willing to make a much riskier foray into real estate investing, you can take the next two strategies.

Real estate investing #2: Rent out properties

Renting out property seems simple enough:

Buy a house or apartment building.

Rent out the rooms to tenants for a nominal fee.

The rental checks come in like gangbusters each month while you sit on a beach in Cabo sipping pina coladas and making passive income.

Hell, that DOES sound awesome — but it’s also complete oversimplification. In fact, renting out property is anything but relaxing. That’s because you’re responsible for all facets of the building you’re renting out as the owner. That includes repairs, maintenance, and chasing down tenants who don’t pay your rent.

And god help you if they do miss a rent payment. If that happens, you’ll have to find another way to pay your monthly mortgage payment.

You CAN make money from renting out properties (many people do!). It’s just that doing so can negatively affect your finances in a BIG way. Check out our house poor article for a good example of that.

If you’re interested in purchasing properties to rent out, be sure to check out the seven-part series on real estate investment basics by Owen Johnson (more on this later). You can find the first article here.

Real estate investing #3: Flipping properties

So you were on your seventh episode of your Fixer Upper binge-watch session and it occurred to you, “Hey, I can do this too!”

By purchasing a house or other piece of property and then renovating and selling it (i.e., “flipping” a property), you can flex your creative and business muscle at the same time…

…but it’s also harder than launching your car into space.

Unless you’re Elon Musk, I guess.

Not only do you have to have the money to buy the property but you also need to be incredibly accurate in terms of the finances that go into the renovations you want to put into the home if you want to make a profit.

That includes things like finding a contractor, estimating the cost of repairs/renovations, and being willing to take the dip in your finances while you try to find a buyer. After all, the longer you hold on to the property, the more you lose in mortgage payments.

BONUS: How to buy a house — real estate investing basics

If you’re really prepared to put in the time to learn about real estate and make sound decisions, check out this seven-part series on real estate investment basics by my friend Owen Johnson. It’ll help you reap the rewards if you decide you’re cut out for it.

Of course, this is just the beginning. I suggest you have intermediate knowledge of real estate before you make your purchase.

I’ll be honest though: I think many people who invest in real estate are making a bad investment. It’s only exacerbated by all of the BS out there about owning a house.

Think about it. We’ve all thought about buying a four-bedroom house and a white picket fence on our own slice of the American Dream.

What many don’t realize, though, is that investing in the four-bedroom house can quickly turn into the biggest money and time sink of their lives. In fact, buying a house is just another one of those invisible scriptsthat we blindly follow without giving it a second thought.

Invisible scripts are those guiding beliefs that are so deeply embedded in our day-to-day lives that we don’t even realize they’re there.

And buying a house is one of those scripts — despite the fact that it’s one of the biggest, life-altering decisions you can make.

In fact, I receive emails every day from people saying, “I have a horrible financial problem. Plz help!” and 40% of the time, it’s directly related to their mortgages.

In chapter 9 of my New York Times best-selling book, I’m hyper-critical of people buying real estate because they think it’s a “good investment” or because they think they’re “throwing money away on rent.”

Those myths — and many others — are just that. Myths. And they’ve been so detrimental to many people’s financial situations that I feel like I need to dispel some of them today.

Here are the four myths of real estate you need to know before you even think about buying a house.

Real estate investing myth #1: “Purchasing real estate is a great investment”

One thing I always hear from people who are about to buy a house is, “Buying real estate is an investment! One day this house is going to be worth WAY more than it is now.”

Look, I get it. We’re always hearing stories from old farts who bought their homes way back in the Truman administration for just $30,000 and now it’s worth $450,000 or whatever.

When the truth is the people who say things like this don’t account for the invisible factors like inflation and maintenance.

Yale economist and Nobel Laureate Robert Shiller reported that from 1890 to 1990, the return on residential real estate was just about ZERO after inflation.

“Take 1/20th of the down payment amount. Start a business.

Your investment might go to zero (which it might also do with a house) but it might also go up to 10,000% returns.

Eventually, as an entrepreneur, if you are persistent enough, you will get one of those 10,000% returns. And you will be persistent because you didn’t waste all the money and time that a house would’ve cost you.”

Real estate investing myth #2: “I’m throwing away my money if I keep renting!”

A reader once told me, “Ramit, I pay $1,000/month renting my apartment, so I definitely can afford $1,000 a month on a mortgage and build equity!”

So I asked her, “Well, how nice is your apartment?”

She admitted that the hardwood floors were old and the kitchen was very outdated.

“So will you want a house like that,” I asked, “or will you want a nicer place — one with recessed ceilings, newer appliances, and a balcony large enough for entertaining?”

She looked at me as if I were an idiot. “Of course I want a nicer house.”

“Okay,” I replied. “But that will cost more than your current rent, right?”

When I said that, a lightbulb went off in her head. She hadn’t even considered that.

Chances are people who want to buy a house haven’t either. Of course, you’ll want a nicer house than the apartment you’re currently renting — ESPECIALLY if you’re committing yourself to a long-term investment like a mortgage. But that means your monthly payment will be higher.

Of course, that seems pretty obvious — but it’s only the beginning.

What many people often ignore when they say that they don’t want to throw money away on renting are the Phantom Costs.

Toilet drains breaking randomly at 2 am forcing you to awkwardly ask your neighbor if you can use their bathroom before you spend a few hours Googling “24-hour plumbers”

These costs will add hundreds per month to your living expenses.

After all, you’re not just paying the mortgage each month. You’re also paying for the oven if it breaks down, or the hot water heater if it isn’t working, or that cockroach problem you inherited from the previous owner.

When you rent, you can just call your landlord if any of those things happen, and he or she foots the bill.

(By the way, the common response here is: “Landlords factor all of that into your rent. They wouldn’t rent out their place if they couldn’t make a profit!” This is incorrect. Landlords don’t charge what their cost is + a profit. Landlords charge what the market will bear. Some make a profit, but many of them are losing money each month.)

When you own, though, you have to fix those things or call someone else to fix them for you. And of course, that comes out of your own pocket.

Sure, the plumber here and the exterminator there doesn’t sound that bad … but imagine that in the course of owning a house, your roof breaks. All of a sudden, that’s $25,000 you need to invest in repairs.

So even if you have a mortgage that is the same as your rent — let’s say $1,000 — you still need to add 40-50% to that monthly amount to factor in the phantom costs. Now you’re paying closer to $1,500/month.

Check out this graph. It shows the true cost of buying a home over 30 years.

If you purchase a $300,000 house today, over 30 years, it could cost you almost $1 MILLION.

In the end, you’re not throwing your money away by renting — but you will throw your money away if you buy a house without knowing what you’re doing.

In the video below, I break down the myths of renting vs buying a house a bit more. Check it out.

Real estate investing myth #3: “If I cut back on enough avocado toast I can afford a house!”

Real estate investing myth #4: “I can always leverage this house or take advantage of the tax savings”

This is effectively two myths in one — but they both boil down to one idea: People think they can guarantee that they will make money by investing in real estate.

I’m talking about leverage and tax savings, and BOTH can cause you to lose money.

Leverage

So many homeowners point to leverage as a key benefit to their real estate investment.

For example, you can put $20,000 down for a $100,000 house, and if the house climbs to $120,000, you’ve effectively doubled your money.

That sounds great, but it’s ignoring one big thing: The price of a house doesn’t always increase (*cut to people who purchased a house in 2007 crying and nodding*). So unfortunately, leverage can work against you if the price goes down.

If your house declines by 10%, you don’t just lose 10% of your equity — it’s more like 20% once you factor in the 6% in realtor’s fees, closing costs, new furniture, and other expenses.

You need to be prepared to face this potential loss before you drop several hundred thousand dollars on a new house.

Though you can deduct your mortgage interest, people forget that they’re saving money that they ordinarily would never have spent.

Think about it. The amount you pay out owning a house is much higher than you would for any rental when you include all those phantom payments I mentioned. So even though you’ll certainly save money on your mortgage interest through tax breaks, the net is usually a loss.

At the end of the day, both leverages and the tax breaks you get from buying a house just aren’t good enough reasons to justify investing in real estate.

So when IS a good time to buy a house?

When you should actually buy a house

Warning: This is going to get a little bit complicated.

To know exactly when the right time is to purchase a house involves a lot of analytics and hours slaving over spreadsheets and “A Beautiful Mind”–style chalkboard equations.

You ready? Here’s when you should actually buy a house:

When it’s right for you.

The fact is there isn’t a right time that fits everyone. Your invisible script is going to tell you that you should buy a house after college or when you’re ready to start a family — when the truth is the right time is as different for you as it is for the next guy. And it may not even be for financial reasons.

Hell, there might not ever be a right time. And that’s okay too.

However, if you are genuinely interested in investing in real estate, I do suggest you do a LOT of research before you jump into anything.

Here are a few GREAT resources I recommend if you’re thinking about buying a house:

The Bogleheads’ Guide to Investing:This is a great website filled with a lot of helpful advice regarding all things investing, including real estate. It’s inspired by the teachings and philosophies of Jack Bogle, the founder of Vanguard

Fixed rate vs adjustable rate:An article I wrote a while back examining why people still take the risky route when purchasing a house

In the end, purchasing real estate might be right for you and it might not. But do not make the largest decision of your financial life because it’s something you “should” do.

What you should invest in

In general, buying real estate is NOT a great investment for individuals.

Instead, I recommend conservatively investing in the stock market via index funds.

By investing in sensible, long-term investments, you’ll have a balanced portfolio that’ll earn you thousands well into your life.

And the sooner you start, the easier it is to get rich.

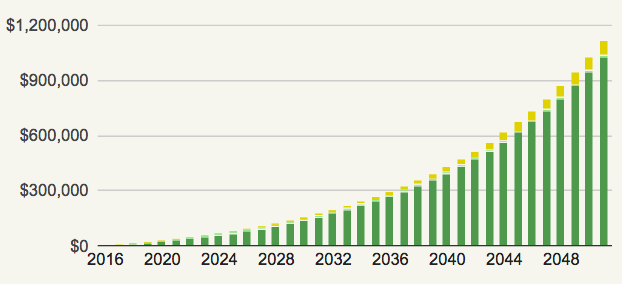

Still don’t believe me? Let’s look at another real world example.

Say you’re 25 years old and you decide to invest $500/month in a low-cost, diversified index fund. If you do that until you’re 60, how much money do you think you’d have?

Take a look:

$1,116,612.89.

That’s right. You’d be a millionaire after only investing a few thousand dollars per year.

Notice, I’m not talking about the Hollywood type of investing where hotshot stock brokers make huge multimillion dollar trades while yelling “SELL” into a phone for some reason.

I said you should invest in low-cost, diversified index funds over time. That’s because smart investments are about consistency more than anything else — not chasing hot stocks. Or other weird investments:

Only through smart investments can you live a Rich Life.

And I want to help you get there. That’s why I’d like to offer you something that’ll help you turbocharge your investments:

My 12-minute video on automating your finances

This guide will help take out the pain of actively investing your money each month. I’ll walk you through the EXACT step-by-step process of setting up your automated finances. By the time you’re done, you’ll be saving AND earning more money passively.

Enter your information below and I’ll send you my free video straight to your inbox.

For instance, if your credit report says that you were late on your payments when you actually paid them on time, that affects nearly a third of your credit score, since 30% of it is determined by the amount you owe.

That’s why it’s so important to dispute any errors you find on your report.

With so many credit report dispute letter scripts out there, which do you choose?

This one:

Hello,

I want to dispute the following information in my file. The items I dispute also are encircled on the attached copy of the report I received.

X is wrong because Y. I have attached a receipt showing this.

A is wrong because B. On December 21st, I sent an email (“Correct my record”) requesting the change.

C is wrong because D.

I have also included my payment records. Please make sure that these errors are rectified soon.

-Ramit

BUT let’s take a step back and get a bird’s-eye view of this letter, why it works, and the exact steps you need to take in order to dispute errors on your credit report.

How to dispute errors on your credit report (with scripts)

I asked my readers how they improved their credit scores a while back — and disputing errors on their credit reports was one tactic that kept coming up.

You can turbocharge your credit score by finding and disputing the errors in your credit report.

The process is going to be fraught with tense negotiations, countless emails sent, and late nights slaving over a hot spreadsheet while screaming into a telephone with your credit card company’s outsourced customer support line.

To dispute any errors on your credit report you must first get your credit report.

Your credit report is an all-inclusive record detailing your credit history and information such as your:

Loan history

Accounts opened and closed

Payment history

Credit balance

Credit bureaus issue your credit report based on information they receive from “data furnishers,” or creditors you’ve worked with (more on this later).

There are three major credit bureaus that will provide credit reports for you:

These are the primary credit bureaus — and the same ones that creditors, lenders, employers, and even potential landlords use to make sure that you’re good about paying back debt on time.

If your credit score is good (700+), you are fine just checking your credit report once a year.

If you find yourself with bad credit (<700) or if you think you’ve been unjustly denied anything due to your credit score, though, you’ll want to get your credit report to dispute anything erroneous in there.

NOTE: If you’ve already used up your free credit report for the year, you’ll still be able to attain it — you’ll just have to pay a fee through the specific credit bureau.

Sites like Credit Karma will allow you to view your TransUnion and Equifax credit report for free. However, in exchange, you’ll have to view advertisements for their credit offers.

When requesting your credit report, you’ll fill out a form online that includes basic information (name, address, DOB, etc.) and also your social security number. Once the form is filled out, you’ll send that information in and receive your credit report in minutes.

Alternatively, you can also order a physical copy of your report by calling the toll-free number 1-877-322-8228. You’ll be asked to provide the same information as if you did it online.

If you ordered your credit report via phone, you’ll receive a copy of it “within 15 days of receipt,” according to the FTC.

If you ordered your credit report through the website, though, you’ll be able to view your credit report right away.

BONUS: Check out this quick video I made a while back explaining how you can check your credit score and get your credit report.

Once you receive your report, it’s now time to find any and all errors that might be in there.

Step 2: Find any errors

A credit report error is simply anything that’s wrong in your credit report. That means making sure that everything on your credit report accurately reflects your actions as a borrower.

Identity errors. These are any issues with erroneous identity. Example: The report got your name or address wrong, they mixed you up with a person with your name, or even cases of identity theft.

Incorrect reporting of account status. These are errors within your individual accounts. Example: When the report says you have an account closed/open when it isn’t, it says you were late on an account payment when you weren’t, or when they report the same debt multiple times.

Data management errors. This happens when you’ve disputed your credit report already and the same errors appear on your next report. Example: You’ve sent a credit report dispute letter about an account you’ve already closed but your next report still contains the error.

Balance errors. It shows the wrong balance in your accounts. Example: It says you owe $500 when you really owe $300.

Identifying these errors is crucial to your credit report dispute letter. So go through your credit report, line by line, and note any and all errors you find.

And there’s no one way to do this. You can print out the credit report and mark it up with a pen and highlighter, or you can just go through it and make notes in a notebook or a Google Doc. Any method works as long as you note all of the errors.

Once you’ve found all of the errors, it’s now time to draft your credit report dispute letter.

Step 3: Send this credit report dispute letter script

Now it’s time to use that email script I gave you at the top.

This one:

Hello,

I want to dispute the following information in my file. The items I dispute also are encircled on the attached copy of the report I received.

X is wrong because Y. I have attached a receipt showing this.

A is wrong because B. On December 21st, I sent an email (“Correct my record”) requesting the change.

C is wrong because D.

I have also included my payment records. Please make sure that these errors are rectified soon.

-Ramit

A few notes:

Just get straight to the point. Just like when you’re writing a cover letter or your resume, each word needs to earn its spot on the page. Your credit report dispute letter should be the same. No messing around. Just get straight to the damn point!

Give them their exact errors with evidence. Note exactly what you are disputing and provide evidence to make your case. Be as comprehensive as you need to be and include specific dates, payment amounts, and account names.

Enclose your copy of the credit report. Include your own copy of the report wherein you’ve highlighted the errors. If you’ve already marked up your own copy of the report for step two, this is a perfect place to send in your handiwork.

Also, remember to keep a copy of the credit report for your records. If there’s another data management error in the future, you’ll be able to use it to dispute the error.

Now it’s time to decide where you want to send your credit report dispute letter. You have three options:

The credit bureau

The data furnisher

Both

Guess which one will increase your chances of having the dispute work?

If you want to send your credit report dispute letter to a specific credit bureau, here are the links to exactly where you can send your dispute.

If you want to send your credit report dispute letter to a data furnisher, you’re going to have to handle that yourself since it’s specific to you and your financial situation.

Once you’ve sent in your credit report dispute letter, it’s time to play the waiting game (everyone’s most favorite game of course).

Step 4: Receive the credit report dispute results

Luckily, you don’t generally have to wait too long. The Consumer Financial Protection Bureau requires credit bureaus and data furnishers to “investigate the dispute within 30 days of receiving it.” After completing the investigation, they have five days to send you the results.

However, there are a few things to note:

If you send in additional pieces of information regarding the dispute during the first 30-day investigation, they can extend it for 15 more days.

They have 45 days if you send in your credit report dispute letter AFTER receiving your free yearly credit report.

Once the investigation period is up, though, congrats! You’ve successfully disputed with the credit bureaus using a great credit report dispute letter!

You’ll now receive a few things. First, you’re going to get a complete summary on what the credit bureau discovered and the actions they decided to take to rectify the errors.

If they decided that what was in the previous credit report was correct, then they’ll tell you that as well.

The credit bureau will also send you a brand new updated copy of your credit report (Note: This is NOT your annual free credit report) and you can frame it and put it on your office wall so you can let everyone know how much of a weirdo you are. I like to put them on my mantle like hunting trophies.

What to do if your credit report dispute didn’t work

You might run into a case where your credit dispute didn’t work and you didn’t get the changes you wanted reflected on your report.

It typically means that the issue you were trying to report wasn’t actually an error when this happens — and that’s okay. There are still many different ways you can improve your credit.

Here are a few resources you can use to get started doing that today:

Getting out of debt and improving your credit score is crazy important. I cannot stress that enough.

There’s a reason it’s on the second rung of my ladder of personal finance.

To help you even more, I’d like to offer you something: The first chapter of my New York Timesbest-seller “I Will Teach You to Be Rich.”

It’ll help you tap into even more perks, max out your rewards, and beat the credit card companies at their own game.

I want you to have the tools and word-for-word scripts to fight back against the huge credit card companies. To download it free now, enter your name and email below.

Your credit score is the biggest determining factor for your mortgage.

Lenders look at other things like your income and job history, but none of that matters if your credit score is in the toilet. That’s why knowing the score you need for a mortgage is the first step in buying a house.

What is that credit score though? The score you need to hit to be able to qualify for most conventional mortgages?

At a minimum: 620.

BUT(of course) it’s a bit more complicated than that. The minimum credit score can vary depending on your specific financial situation, your debt-to-income ratio, and which mortgage you choose.

The different types of mortgages

The world of mortgages can often feel like the Wild West — a dramatic and confusing place with unwritten rules that can end your journey at any second. Only those with grit (and a high credit score) can survive.

And in this chaotic land, there are two kinds of mortgages you can get. They are:

Conventional mortgage. These mortgages are insured by private lenders. The biggest of which are the Federal Home Loan Mortgage Corporation (Freddie Mac) and the Federal National Mortgage Association (Fannie Mae).

Government mortgage. These are mortgages that are insured by specific government agencies.

Future homeowners also have the option to choose between three different types of loans within government mortgages. Those are:

FHA loans. These loans are insured by the Federal Housing Administration and given by a private mortgage lender. These mortgages are popular because they require a small down payment when compared to other types of home loans. It’s also much easier to qualify for these loans if you have less-than-perfect credit.

VA loans. These loans are insured by the Department of Veteran Affairs. As such, they’re only available to military service members (active or discharged). They’re very lucrative to prospective homeowners due to their incredibly low to no down payment.

USDA loans. Aside from making sure your steak is “Grade A” Angus beef, the Department of Agriculture also doles out home loans for rural areas. These loans are tailored for low-income homeowners and don’t require you to pay mortgage insurance.

Your credit score will be the biggest determining factor on whether or not you get these loans.

So let’s take a look at how different credit scores can affect your mortgage (in classic spaghetti western fashion):

Having a credit score in the 700 range is the good. It shows lenders that you’re the Clint Eastwood of borrowers — competent, reliable, and deadly in a Mexican standoff.

In fact, you might want to aim it even higher than that.

“You should aim to have your credit in the high 700s if you want to be absolutely ensured a home mortgage,” says Jasmine, a home mortgage advisor at MortgageAdvisor.com. Her job is to help would-be homeowners understand exactly what they need in order to secure a home loan, so she knows her stuff.

According to Jasmin, this puts yourself into prime position to obtain a mortgage without worrying about being denied due to your credit score. This applies to both conventional mortgages as well as government mortgages.

Having a credit in the high 700s is also beneficial because it means you’ll likely get a better interest rate on your mortgage too. This could mean saving thousands over the life of your mortgage (more on that later).

So having your credit score in the 700s is the good … but what about the bad?

Credit score for mortgage: The bad

620 is bad. Mortgage lenders will likely approve you for a loan — though they’ll be suspicious of you and your dastardly ways.

Luckily, it’s not the worst credit score for mortgage. 620 is just the minimum credit you’ll need to qualify for most conventional mortgages with private loan companies like Freddie Mac or Fannie Mae.

“At a minimum, you have to be at least at a credit score of 620 [for conventional mortgages],” Jasmine says. “If it was below that, you would have better luck of applying for an FHA or a VA loan.”

That’s because the credit score minimum for government loans tends to be lower and occasionally non-existent (with the exception of USDA). Take a look:

Just because this is the minimum credit score doesn’t mean that this should be your goal credit score though. Your credit score affects aspects such as your interest rates as well as your initial down payment.

For example, if your credit score is 500 and you’re applying for an FHA loan, you’re going to need to put down a 10% down payment on your home as opposed to 3.5% down payment if your credit score was 580 or higher.

So that’s the bad credit score for mortgage. Let’s take a dive into the dark pit that is the ugly credit score.

Credit score for mortgage: The ugly

Oof. At less than 500, your credit score looks sorrier than a steer in a stockyard. You best high-tail it towards our articles on improving your credit score to help you out … ‘cause you got a score not even a mama could love.

There are still ways to get a home loan if your credit score is less than 500 (such as getting a VA loan). However, you’re going to want to improve that credit score if you want a good interest rate and low down payment on the house.

This can end up saving you thousands over the length of your mortgage.

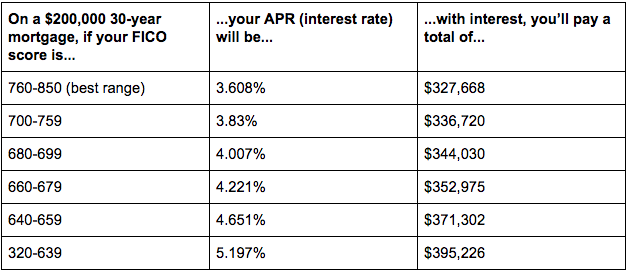

Imagine two home buyers. One has a great credit score of 760 and the other has a bad credit score of 500.

The one with the bad credit score is going to end up paying over $67,000 more in interest than the one with fantastic credit.

Don’t be the one with an ugly credit score. Instead, start taking steps to improve your credit score today.

How to improve your credit score for mortgage

If your credit score is bad then you’ve come to the right place, partner. We have a wealth of resources at IWT to help you get out of debt and improve your credit score faster than a jackrabbit in a hurricane — or something.

Anyway, here’s a quick overview on our proven system to improving your credit score:

Step 1: Get out of debt fast. Debt is the number one barrier to living a Rich Life. That’s why if you want to improve your credit score and get a Big Win, you’re going to want to get out of debt as fast as possible.

Step 2: Automate your credit card payments. The biggest determining factor of your credit score is your payment history. That’s why you’re going to want to automate your personal finances so you can do things like invest and pay down debt easily and painlessly. It also takes the hassle out of paying your bills each month.

Step 3: Keep your accounts open — and put a recurring charge on them. 15% of your credit score is determined by the length of your credit history. That’s why you’re going to want to keep any credit card accounts open BUT keep just one or two recurring payments on them (e.g., Netflix, utility payments, rent).

Step 4: Get more credit — but only if you have no debt. 10% of your credit score is determined by how many types of credit you have in use. That’s why you’re going to want to actually get more credit once you’re out of debt.

To help you even more, we’d like to offer you something: The first chapter of Ramit’s New York Timesbest-seller “I Will Teach You to Be Rich.”

It’ll help you tap into even more perks, max out your rewards, and beat the credit card companies at their own game.

It includes the tools and word-for-word scripts to fight back against the huge credit card companies. To download it free now, enter your name and email below.

Koho is a Canadian spending and saving app that gives you insights into your spending behavior while helping you meet your financial goals. This review is NOT a sponsored blog post, but I do have a special affiliate code with Koho. If you use the code BRIDGET10 when you sign-up and activate your card, you’ll get a free $10 (and I’ll also get $10). Set up a direct load from your paycheque to your Koho card, and you’ll get an additional $40! Once you’re signed up, you’ll receive your own code to invite friends & family and also receive the same bonuses when they sign up. A half-dozen subscribers asked me about Koho, and I figured the only way to give an honest answer was to try it out myself. At first, I didn’t get it. I really thought it was more or less a pre-paid Visa attached to an ordinary […]

Ahhh! Enough with the same old boring posts about engagement rings!

Yes, we know the diamond industry wants us to spend more. Yes, De Beers is evil, and yes, synthetic diamonds are flooding the market, and yes, I saw “Blood Diamond” with Leonardo DiCaprio. And yes, we know about your aunt’s cousin’s brother who got a ring for $2.59 and they’ve been happily married for 80 years.

That’s great.

But when I decided to propose to my girlfriend, I started doing research — and I found myself getting increasingly frustrated. I had real questions.

What type of ring should I get? Do the “4 Cs” really matter? Is this jeweler going to rip me off? Do I really need to save two months’ salary?

I did a quick Google search and I felt myself getting even more frustrated. The advice on other sites told me to “do my research,” “find out her ring size,” and “pick my budget.”

Uh … I ALREADY KNOW THAT! No one addressed the real questions I had.

So, I did my own research and now I’m going to show you exactly what I ended up doing, including:

The exact word-for-word conversations I had to get on the same page with my girlfriend about the kind of ring she wanted

How I navigated the “cost” issue — including what I discovered about what really matters when buying a ring

What I learned from an NYC Diamond District jeweler who broke the diamond industry down for me

This is the stuff you won’t find in other engagement ring posts.

Hi, my name is Ramit Sethi. I’m the author of a New York Times best-selling book on personal finance. Don’t worry, I’m not going to make you feel bad about wanting to buy an engagement ring (or even spending a lot on it). I don’t have any secret backroom deals with diamond dealers. I just want to show you what nobody else is talking about when it comes to buying an engagement ring.

I spent a huge amount of time learning about the diamond industry and ended up buying a ring that my girlfriend Cass — now fiancée — loved.

Here’s what I knew going into the process: I’d met a woman I loved and I knew that an engagement ring was important to her. She never mentioned size or cost, but I knew she wanted a nice ring that was ethically sourced.

This is my personal experience finding the perfect ring for her with some additional insights from you guys, my readers.

So here we go…

The 1 thing that matters above all else

In my life, I have discovered one solitary truth:

Every single comment about engagement rings focuses on saving money. Always.

In ANY article about engagement — no matter which site, which author, which date — 99.99% of comments will say, “LOL! Buying an engagement ring? I spent $0.32 and we’ve been married for 43 years!”

Guys, there are plenty of ways to save money on a ring. You can find them on 50 million other articles where people race to the bottom of how little they spent, then brag about it.

But I have another view:

Your engagement ring is a unique gift, which you — in consultation with your partner — decide on.

If you want to spend $100 on a ring, great! If you want to spend $50,000 on a ring, and you can afford it, also great. Some people prefer a ring that was passed down from their mother. Others prefer an ultra-modern ring, or a heritage design, or an oval shape. I know a guy who spent $300 and I know a guy who spent $100,000 on his engagement ring. Both have great marriages.

In other words, I don’t believe in focusing solely on the price — I want to focus on the value of your gift, which ultimately only you decide. You should consider what your partner wants, but ultimately you decide. Not your friends, not society, not De Beers, and certainly not some random frugalista commenter on the internet.

So I knew I wasn’t going to focus on finding the cheapest ring. I was going to find the ring that was perfect for my fiancée. Here’s how I did it.

What to do before you buy

Until I got deep in the process, I didn’t truly understand the sales mechanisms that the industry has created to encourage you to spend more. These include creating their own rating system (the 4 Cs: cut, color, clarity, and carat), creating their own governing body (GIA), and even their own set of rituals and phrases (“A diamond is forever”).

Wait a sec. Is this a religion? Or buying a commodity?

As one friend told me, “I didn’t know what I was doing, but I knew I was doing it wrong.”

I realized that 80% of the work is done before you set foot in a jewelry shop. If you just walk in and say, “Uhh, I’m not sure … what do you recommend?” then you’re going to get taken for a ride and end up being one of those guys who gets bitter about the process. Average process, average results.

But if you arm yourself with information, this can actually be fun.

I went a little crazy and mapped out the entire process. Hey, what can I say? I love systems.

The map looked like this:

There are lots of sub-steps beneath each step. But remember the big insight that “80% of the work is done before you ever set foot in the room”? You can see it in the outline: Most of the work — 80% — is done before you ever get to the “Buy ring” step. Get these early steps right, and the rest is just details.

Start from zero

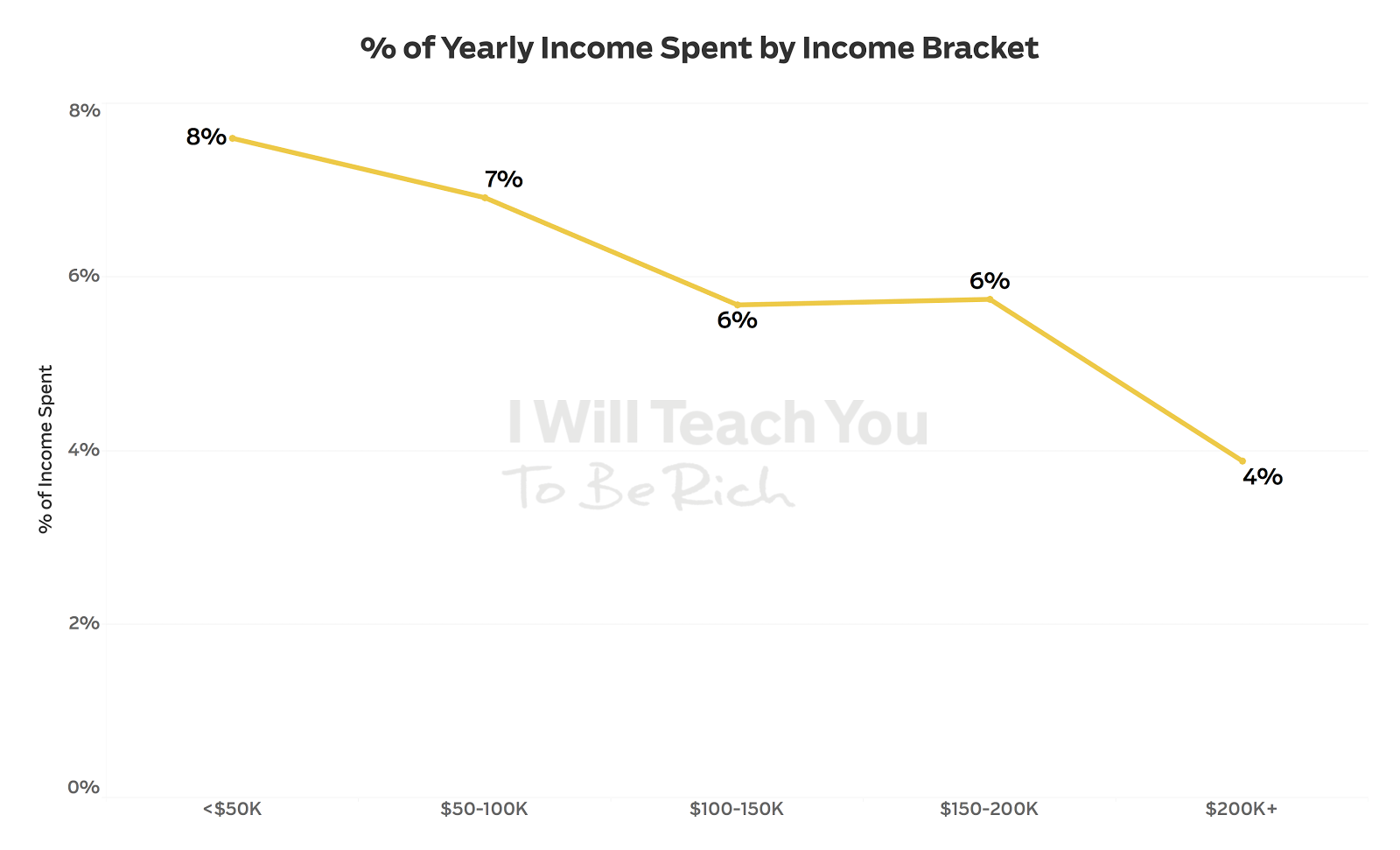

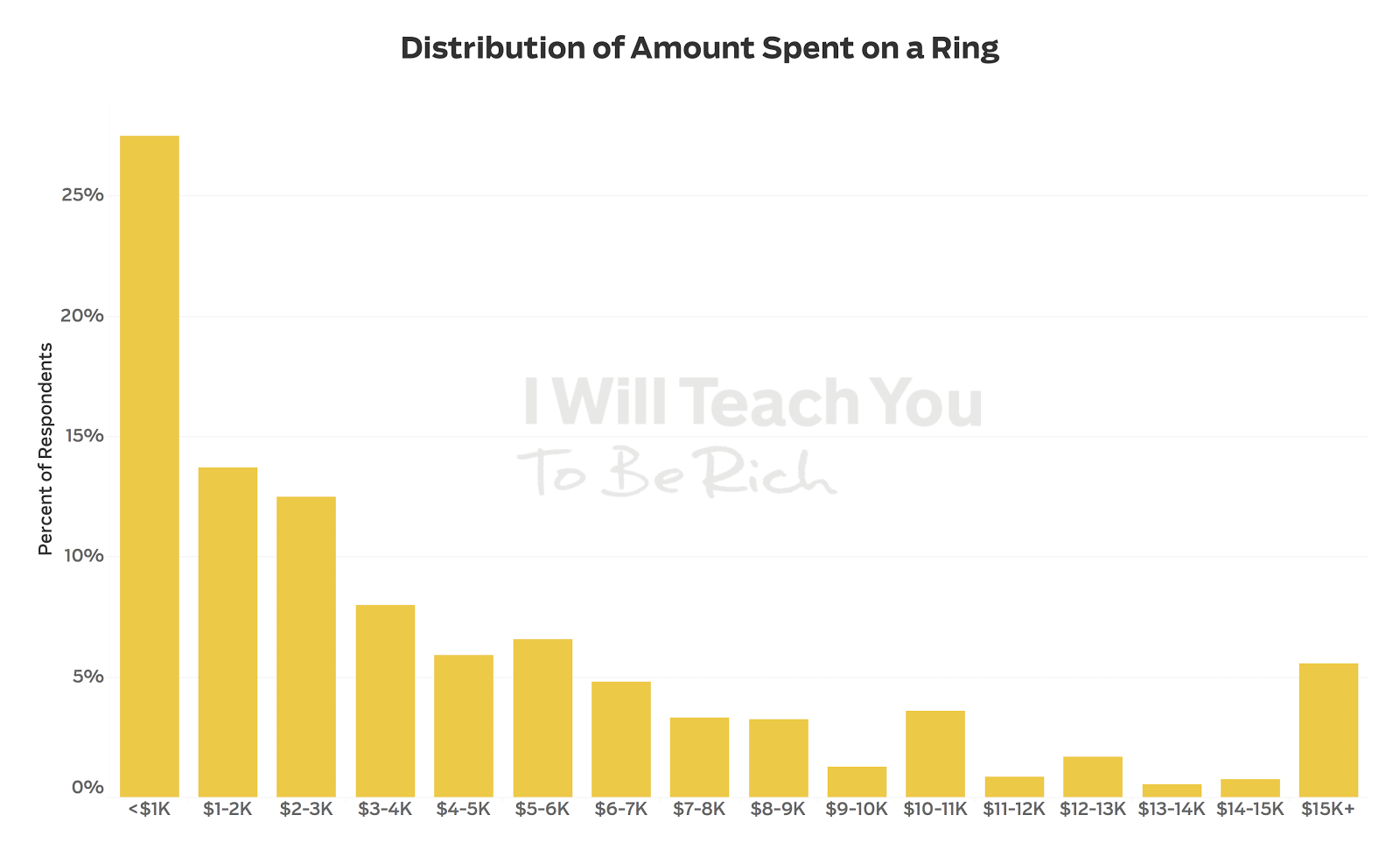

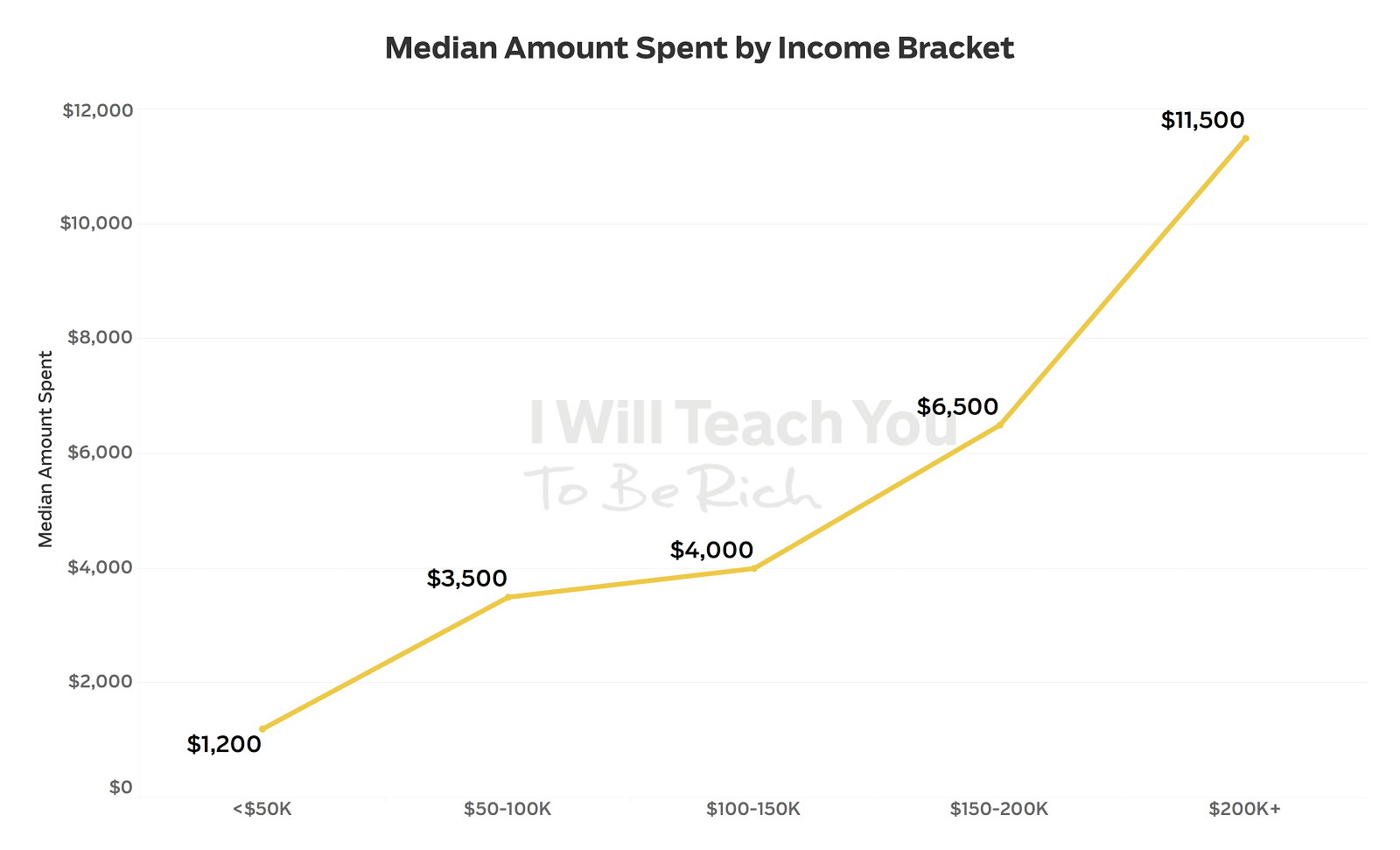

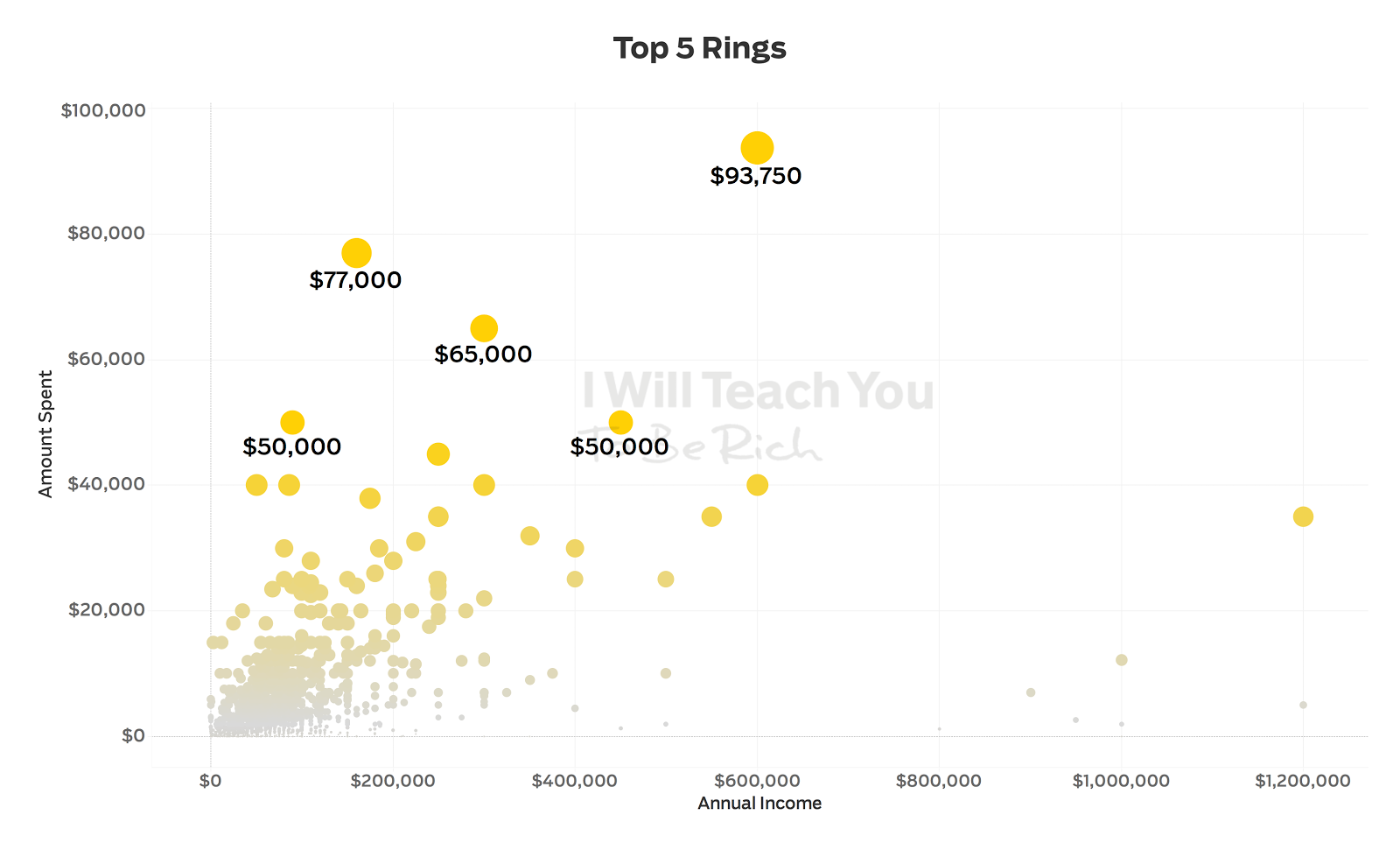

First of all, forget all the bullshit about two months of salary. That is pure marketing nonsense. Look at your own financial situation to decide what you can comfortably afford. I asked more than 1,500 of my readers, and depending on income, people typically spent between 4% and 8% of their yearly income.

So I started with getting a general price down. It could be “$1,000 to $3,000” (with room to stretch to $3,500), or it could be “around $10,000” or even “$40,000 to $60,000.” Whatever it is, know it and remember it.

This data isn’t scientific. But with over 1,500 results, it gives you a general sense of how much people spend. Personally, these numbers seem low for what I know my friends in NYC spent. But this is the full dataset without regard for geography. Click to enlarge.

If you’re having trouble settling on a budget, find your income bracket here for a general benchmark. Click to enlarge.

A general number helps because when you walk into a store, you’re not a mark — you’re in control. You wouldn’t ask a car salesman what kind of car you should buy. You’d do your homework first! Do the same thing for your engagement ring.

Talk to your partner. THIS IS IMPORTANT

Then have the conversation with your partner. (Note: I’m using “her” and “girlfriend” because my fiancée is a woman and I’m a man, but you can apply these same lessons to any relationship.)

Feel free to use this word-for-word script to get on the same page about your engagement ring:

“I really love you and I’m excited to spend the rest of our lives together. I know we’ve talked about marriage already, but there’s actually something I want to bring up that I want to be open with you about: I’d love to talk about the ring. It’s something I’ve been thinking about, and I’m guessing you’ve been thinking about it too.

What kind of ring do you have in mind? Have you thought about the band? I’d love to hear what you think.”

Things I did in the conversation:

I made sure to contextualize the ring as something we were doing together

I also made sure to be friendly and open

I didn’t bring any chips on my shoulder (e.g., anxiety about budget concerns) into the discussion

The big insight here is to actually ASK THE RIGHT QUESTIONS about the ring. Or, frankly, any questions at all! It’s amazing how many guys go into the ring-shopping process without knowing anything about what their partner wants. You knuckleheads create your own stress and anxiety — all because you’re not willing to open up the conversation and ask.

Over time, I came to believe part of the reason we’re afraid to talk it out is that many of us — men and women — absorb this Disney-esque invisible script that everything around the proposal should be a surprise.

Feel free to keep the date of your proposal a surprise, how you’re going to propose, even the ring itself — but the fact that you’re going to propose and the type of ring should not be a surprise. Stop being morons and trying to randomly decide on some of the biggest decisions of your lives together! Here are a few important things to talk about: “Do you want a public or private proposal? What color band? What shape? Let’s get on the same page about finances, because that will affect both of us as we build a life together.”

So, have the conversation. The script above shows the importance of your partner’s feelings to you. You’re asking her what kind of ring she envisions — is it oval? Round? Something passed down from your mom? (During the conversation, it’d be a great idea to ask her what her ring size is as well. Just a simple, “By the way, what is your ring size just so I know it?”) By asking your partner questions, you allow them to lead the conversation and create a really positive experience.

Wrapping up the conversation

“I really appreciate that we can be open about this. I’m going to think about it, but I just wanted to say thanks. It’s great to talk about this and I’m excited for this next step.”

OK, the conversation went well, but I’d also planned just in case it hadn’t gone well. What if she’d told me she wanted some ring that was totally out of my budget? Fortunately, I didn’t have to have this conversation — but I was ready just in case:

The backup plan: “What if she wants a ring that I can’t afford?”

“I want to talk to you about something that makes me a little uncomfortable but want to be honest about: From the last time we talked, it seemed like the ring you wanted was XYZ. Am I reading that right?” (Clarifies any misunderstandings you might have)

“I would love to get you the ring of your dreams … but I also want to be thoughtful about our finances as we build our lives together.” (Reiterates how you’re keeping the relationship in mind)

“Based on our budget, I can’t do the one you want right now. But I heard what you’re looking for and I’m going to do my best to find the most perfect ring to signify our relationship.” (Shows that you’re honest about the situation but also considerate of what she wants. Now begin wrapping up)

“Thanks, this was really great. I’m going to think about a few things. I really appreciate having this discussion. It feels really good to know we can have an honest discussion together.”

Ask your fiancée to send you what they like

After my fiancée and I talked, she proactively sent me an email with examples of rings she liked, rings she didn’t, band preference — everything.

I don’t think that’s weird, I think it’s awesome.

This is a gift she’s going to wear for the rest of her life. I want to know what she wants! I want her to be thrilled with it. Be sure to nudge your fiancée to do the same before you go shopping. Below is the email my fiancée sent. I added the yellow boxes and arrows to showcase what’s happening in the email.

Notice the details: color, shape, level of details, etc. This just helped me narrow down my choices in a huge way. Get this information from your partner!!

Size and bling: The only 2 things that matter

OK, now that you have a rough idea of what your partner wants and you’re ready to start looking, it’s time for some diamond-industry truths.

The diamond industry created the “4 Cs” as a way for you to “measure” the value of a diamond. This is a helpful framework to evaluate a diamond — but as soon as you learn it, you will realize how limiting it is.

Here’s what I learned from my experience: When it comes to the diamond, 2 things actually matter: size and bling (the visual appeal — think “sparkle”). In that order.

People get mad hearing this, but you should ask the experts: people who’ve bought diamonds. I remember a bunch of my guy friends at a bachelor party talking about when they bought engagement rings. “Everyone will say they care about all kinds of different parts of rings, but when it comes down to it, size and the bling are the only things that matter.”

Each married guy — guys who had actually bought diamonds for their partners — just nodded and laughed. They all knew it was true.

There’s a lot to unpack here, but I’m intentionally not getting into the socio-political aspects of diamonds. This post is specifically about what I learned buying a diamond.

In short: Yes, you should do your research on the 4 Cs to get a feel for the terminology that will be used by your jeweler. And yes, it’s good to compare diamonds to each other. But ultimately, size and bling (“sparkle”) are the primary things that matter.

This means that the most important aspects of the ring are purely visual. Now that you know the 4 Cs, forget about them. I’ve seen high-grade diamonds that looked duller than low-grade ones. I’ve seen two oval diamonds, both within $2,000 in price — and one looked about $20,000 more expensive.

“Clarity” is the absolute stupidest one of all. It describes tiny micro-blemishes on the diamond (this is where you use a jeweler’s loupe to inspect it). Guys, let’s get real. The naked eye can’t see these blemishes — and you will never use a loupe in real life — so it’s pointless to weigh this in your purchase.

As one jeweler told me, “You should get educated about the 4 Cs. But using cut and clarity is like buying a calculator based on its length and width.”

Call it the “Instagrammization” of diamond rings. The visual appeal matters more than anything else. If you dig deeper, there are a lot of reasons why: When your fiancée announces the engagement, there will be photos highlighting the ring. The first thing her friends will do is say, “Let me see the ring!” Whether you like it or not, the ring is a social statement. My philosophy is to acknowledge the game being played around you. You can choose whether or not to play, but know the game.

Some people find this distasteful. I found it liberating.

Out of 1,500+ respondents, these are the five most expensive rings. Here they are graphed according to income levels. Click to enlarge.

Think about it — now that I knew the visual appeal mattered most, I could focus my search around the look of the diamond. I could instantly discard most of the nonsense around the “perfect” diamond.

This is an area where you can “capture value,” or save money, since you don’t need to weigh it in your consideration.

So forget about micro-blemishes, the stories you hear about the diamond heritage, and resale value. This is a gift, not an investment. Focus on the two key drivers that people want — size and bling — and get the ring that you and your partner discussed.

In other words:

Use your eyes to judge a diamond your partner will love. Don’t let the 4 Cs lead you astray

In my experience, size and bling (“sparkle”) matter most. Be smart. Don’t buy a big diamond that has no bling. It’s important to balance the two

Above all, be sure you know what your partner wants and loves! Don’t let your preconceived notions (or worse, society’s) guide your decision. This gift is about your partner

By now, you know your budget, the type of ring and band, and you know to focus on size and bling. Time to get the ring.

How I went shopping for the ring

I love the phrase, “Play from a position of strength.” You’re about to make a large purchase — so act like it. Make the salespeople work for you. Be crystal clear with what you want and what you expect. Of course, be polite — but remember you’re playing from a position of strength.

Hey, I know everyone thinks the proposal is all about romance, but I also love LOGISTICS. I’ll show you exactly how I did it.

By now, you’ve had a conversation with your partner about what she’s thinking about when it comes to a ring. You’ve carefully thought about what you want to do and what you can afford. This is amazing — you’re light years ahead of most others.

Now, I’m going to show you how I approached the buying process so you can do a few key things differently.

Step 1: Find 3-5 jewelers and set up appointments

First, I asked a bunch of my male married friends which jewelers I should talk to. The most common response I got was, “I have a guy.” Everyone has a guy. I started to make a short list of jewelers in NYC they had used.